AI-related equities have risen sharply in recent years and now represent more than a third of the S&P 500. But are AI equities in a bubble about to burst, or is the real risk lurking elsewhere? AI is a disruptive technology and differs from the dot-com era by being lower valuated only moderately more expensive than the broader market. As always, the timing of a potential correction is the most intriguing question, and it hinges entirely on collective confidence. That confidence, in turn, depends on a web of underlying factors, among them steady growth, resilient supply chains, and ample liquidity..

AI -related Equities Have Risen More Than Others ...

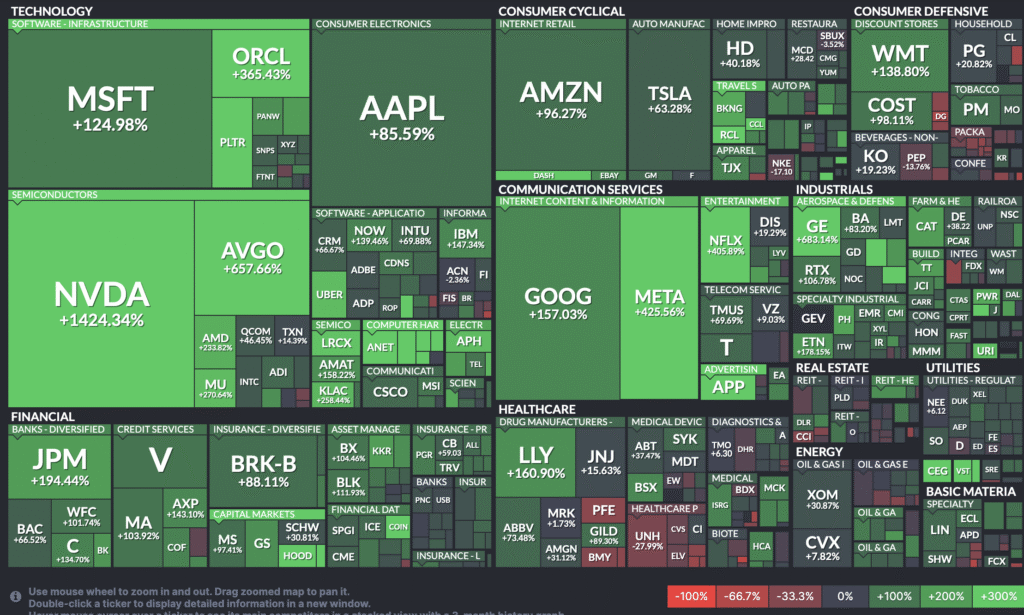

Over the past three years, companies with the greatest exposure to AI have significantly outperformed the broader market.

This has been particularly evident in the case of NVIDIA, which found itself in a product “sweet spot” with its GPU chips. Unlike traditional CPUs, optimised to execute one sequence at a time, GPUs are designed to run thousands of simultaneous processes, making them ideal for AI-related workloads. Over the past three years, NVIDIA’s market value has increased more than fourteenfold and now accounts for over 8% of the total value of the 500 largest US-listed companies.

Similarly, other AI-oriented firms have risen sharply, leaving today’s equity markets more concentrated than at any point in modern history. The ten largest companies in the S&P 500 now represent more than one-third of the index’s total market capitalisation, and of these ten, seven are directly driven by AI development. The remaining few are “merely” influenced by it.

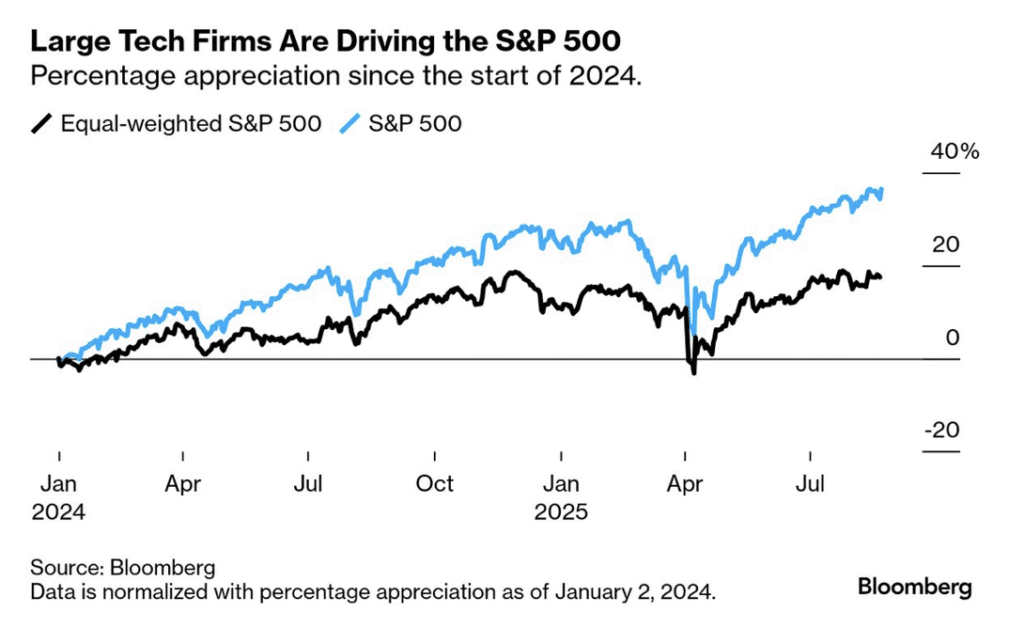

Expectations regarding the economic potential of AI are therefore enormous, and this is why the large technology firms continue to outperform the broader market.

The effects have been felt primarily among hardware producers, such as NVIDIA. The same trend can also be seen for the hardware that will power AI development in the years to come. Among quantum computing companies, market capitalisations remain relatively small, yet in several cases their share prices have risen even more dramatically.

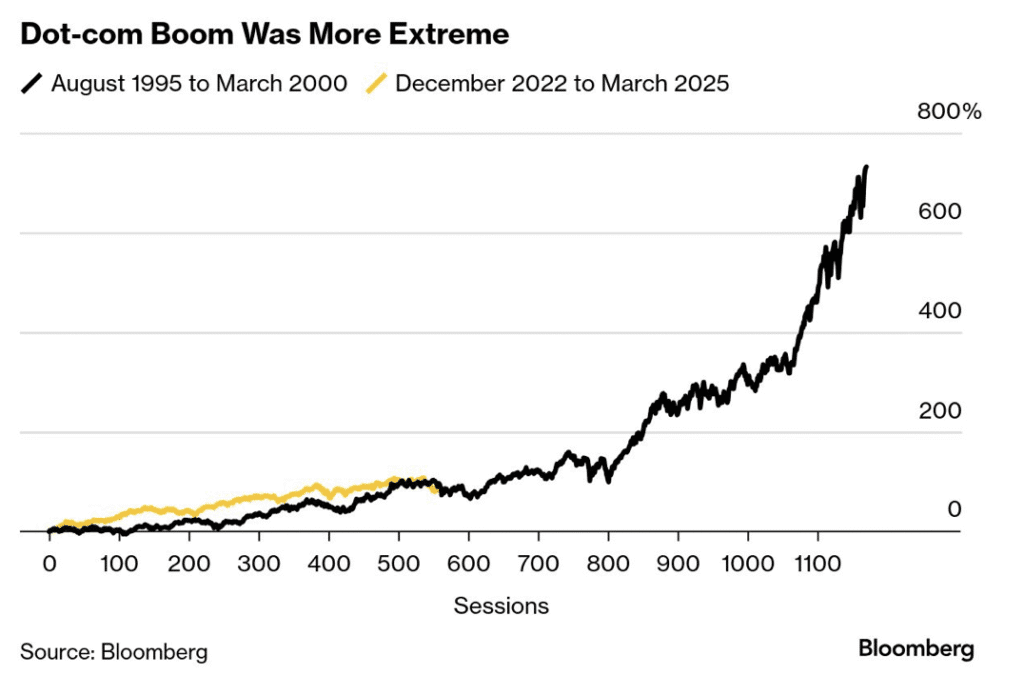

When such sharp increases are driven primarily by expectations of economic gains from a single technology, it inevitably brings to mind the dot-com era.

… But So Too Has Their Growth in Both Sales and Earnings

There are, however, some decisive differences this time: both sales and profits are rising, and the underlying technology exerts a far broader and deeper influence than dot-com ever did.

During the dot-com years of 1999–2000, companies such as Cisco, Yahoo, Sun Microsystems and Amazon often traded at forward P/E multiples of 60 to 120, if they had any positive earnings at all. The market was effectively pricing in the next 50 to 90 years of profit. These extreme valuations reflected a widespread belief that the companies themselves underestimated their true potential.

This differs markedly from dot-com

That situation differs markedly from today:

- Firstly, the forward P/E ratios of AI companies generally sit between 20 and 30, if one excludes outliers such as Tesla. The market has therefore priced in “only” the next 15 to 25 years of earnings.

- By comparison, the average forward P/E for the broader market is around 21. AI stocks are thus trading with only a modest “innovation premium” over the market. In fact, many AI companies trade below stable but defensive names such as Walmart and Costco.

- It is important to remember that AI stocks have only moderate forward P/Es because their earnings are keeping pace with sales growth. Their price increases are therefore more than merely speculative.

- They also generate strong cash flows, which makes these companies financially robust, as their growth is less dependent on fragile external funding. NVIDIA’s cash flow, for example, is so large that it, like OpenAI, effectively acts as a central financier for many purchasers of its chips. Both NVIDIA and OpenAI convert this financial leverage into commercial influence, as outlined below.

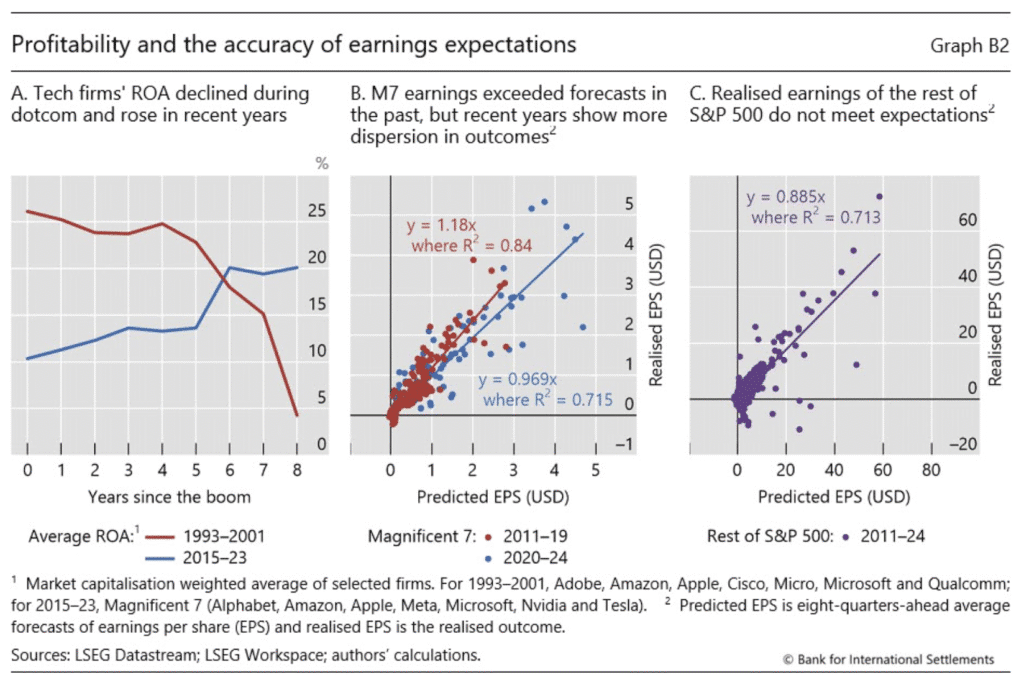

- Finally, AI companies continue to surprise the market positively, both in terms ofsales growth and Earnings Per Share.

The Bank for International Settlements reached a similar conclusion from a slightly different perspective when, in Q3 2024, it examined the parallels between the dot-com era and the current AI-driven growth. It is therefore too early to declare AI technology a bubble on the verge of bursting from within.

For AI Technology Has a Broad And Disruptive Potential …

To put it somewhat bluntly, the dot-com era was based on a technology that primarily streamlined and opened up companies’ distribution channels. By contrast, AI's potential is far broader and far more disruptive.

While the use of large language models (LLMs) today largely “only” enhances efficiency and productivity for a wide range of users, AI’s major disruptive potential lies in research and development. Here, . In itself, this should lead to entirely new fundamental understandings of the world around us..What is new about AI is that it is universally enabling, self-learning and thus exponentially evolving, and that it offers opportunities for deep adaptation. Taken together, it represents a new form of intelligence, rather than simply a faster version of our own.

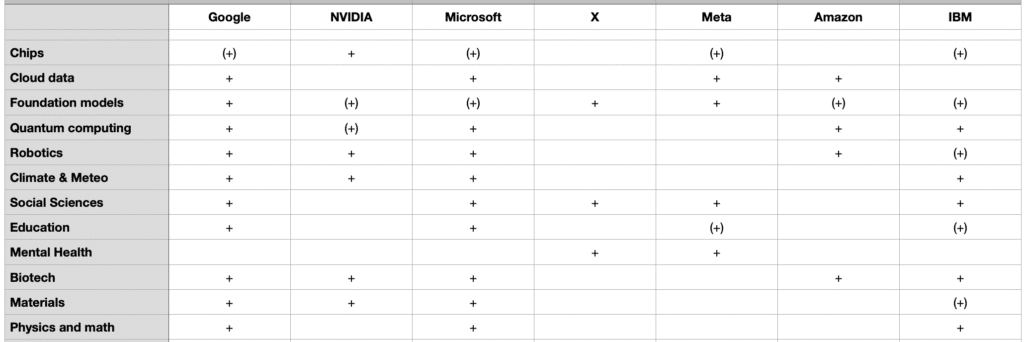

AI companies recognised this potential early on. Consequently, they have long invested strategically in areas where they see the greatest future opportunities, while simultaneously positioning themselves to shape and leverage these opportunities. The broader the AI companies’ investments, the greater the risk diversification they theoretically achieve.

The investment landscape thus looks roughly as follows:

See blog for more detailed descriptions of the commercial potentials.

… In Which AI Companies Have Invested Broadly

The overview suggests a.o. that, although Google and Microsoft were overtaken in 2022/23 by OpenAI’s LLM, ChatGPT, they have diversified into advantageous positions for the future. Both companies already had extensive collaborations with universities and were well established within Silicon Valley’s venture ecosystems. They have leveraged these connections to invest strategically, capturing a share of the substantial AI upside and increased innovation.

The overview also highlights that the current biggest AI winner, NVIDIA, has actively sought to diversify its commercial foundation. This has been achieved through direct investments in areas such as robotics, climate data, biotechnology, and materials development. Additionally, the company’s cash flow has been so strong that it has aimed to consolidate its role in AI development by funding other AI companies.

Such funding concentrations have been seen many times before. They often lay the groundwork for later consolidations among market participants, particularly in the aftermath of a bubble burst. This market dynamic characterised, for example, the pharmaceutical bubble of the 1990s and parts of the dot-com market in 2000. The risk today, however, is that funding has become unusually circular around NVIDIA, Oracle, and OpenAI. This represents a form of systemic shadow-bank debt, which could be triggered if one of the key players becomes illiquid. OpenAI is particularly exposed in this regard, notably through its StarGate project, should e.g. SoftBank withdraw.

The Technology Has Some Critically Sensitive Supply Dependencies

In any equity market, by definition, market prices reflect compromises between supply and demand, since any given share is always owned by someone. Therefore, the market price reflects the average confidence in the future among investors.

Here, however, an interesting sentiment signal emerges: who actually owns the stock. While no investor can predict the market with certainty, large institutional investors generally have better tools and information to do so. They typically make decisions based on broader and more diversified data, processed in a more measured and objective way. This has historically given them a track record of greater long-term accuracy. In the short term though, luck always remains the decisive factor in timing investments.

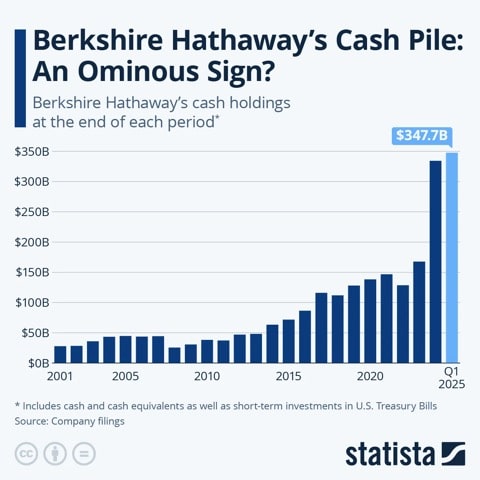

Among the world’s most successful long-term investors is Berkshire Hathaway. Over the past two years, the firm has increased its cash holdings to a record-high level, reflecting its view that the broader market is overvalued. Nevertheless, Berkshire Hathaway remains heavily invested in AI-exposed companies such as Apple, Amazon, and BYD, as well as indirectly in Broadcom, IBM, Microsoft, and Google.

Overall, AI equities are not necessarily in a bubble

Overall, AI stocks are therefore not necessarily in a major bubble, in immediate danger of bursting. This view is reinforced when considering the timing overlap between the dot-com period and the current AI-driven price rises.

That said, AI stocks are by no means risk-free. AI’s success depends e.g. on financial stability and a stable underlying economy. For current valuations to be justified, AI must deliver on its commercial potential. This, in turn, requires uninterrupted functioning of supply chains, including electricity, raw materials (e.g., rare earths), and chips.

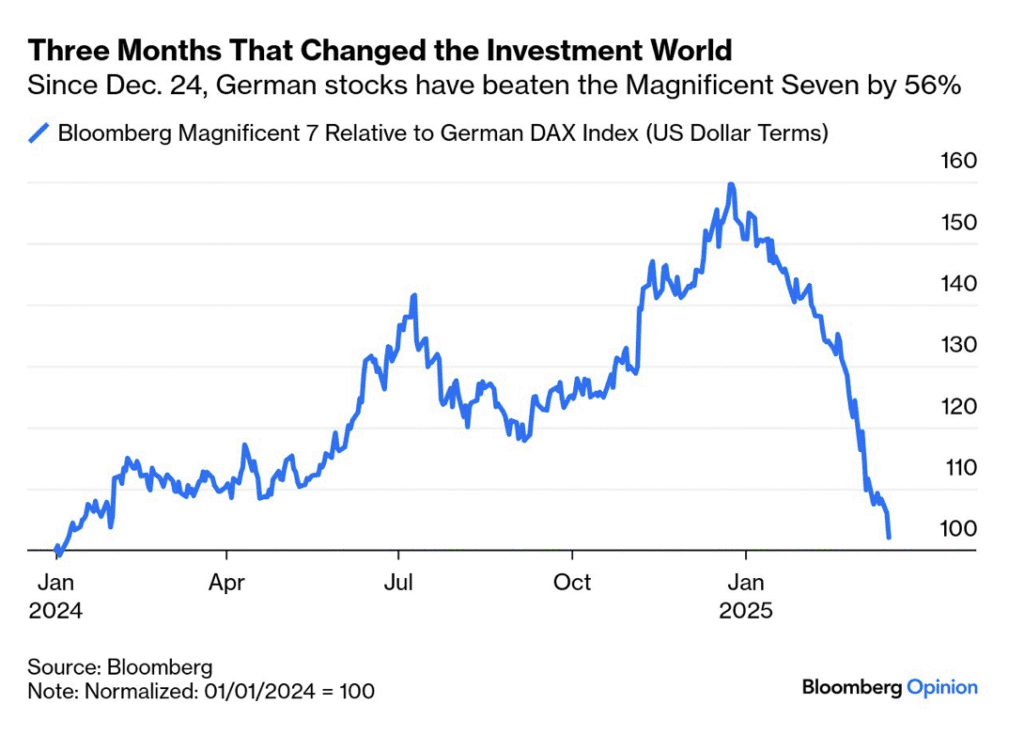

Here, the market has cause for concern. An example emerged at the start of this year, when the Magnificent 7 stocks fell relatively more than heavy industrial equities.

See next week's blog post