AI-related equities have risen sharply in recent years and now represent more than a third of the S&P 500. But are AI equities in a bubble about to burst, or is the real risk lurking elsewhere? A collapse in AI equities would affect the entire world. As always, the timing of a potential correction is the most intriguing question, and it hinges entirely on collective confidence. That confidence, in turn, depends on a web of underlying factors, among them steady growth, resilient supply chains, and ample liquidity. This is part 3 of 3 on the valuation of AI equities.

An AI Equity Collapse Would Affect the Entire World …

The AI bubble is therefore closely intertwined with the US economy. Should a recession occur here, there is a significant risk that AI stocks would collapse. Conversely, there is also a substantial risk that a sudden collapse of AI stocks could itself trigger a recession in the US, given the magnitude of potential value losses.

Most of the largest AI companies are American. The rest of the world has also invested in US-based AI, meaning that a burst of the AI bubble in the US would impact the global economy. The US, as the world’s largest economy, underpins much of global financial stability, largely due to its deep and liquid debt markets, which have given the USD its “exorbitant privilege” as the world’s leading reserve currency.

Furthermore, the economies and financial stability of the rest of the world are affected if the US experiences a recession or rising inflation, since global investors are heavily exposed to US equities across the board.

A sudden collapse in AI stocks could itself be triggered by disruptions to chip supplies, for instance from a Chinese blockade of Taiwan, or if US energy supply fails to keep pace with the massive energy demand from AI data centres.

… But Collapses Usually Follow a Certain Pattern, ...

The risk of a broader recession in the US is currently increasing due to the country’s economic policies. There is typically a recurring pattern for economic slowdowns:

In the first phase, key economic indicators decline but remain mixed.

- There are currently small signs of this. The labour market is cooling , with only modest rises in unemployment, and there is insufficient momentum in the US re-industrialisation to generate new jobs. Only high-tech sectors, particularly AI, continue to grow significantly.

- Real wages in the US are also continuing to fall. This is critical, as over a third of American consumers lack sufficient financial reserves to withstand three to six months of temporary unemployment. Policies such as Trump’s OBBBA risk widening income inequality, which is already at levels comparable to 1929.

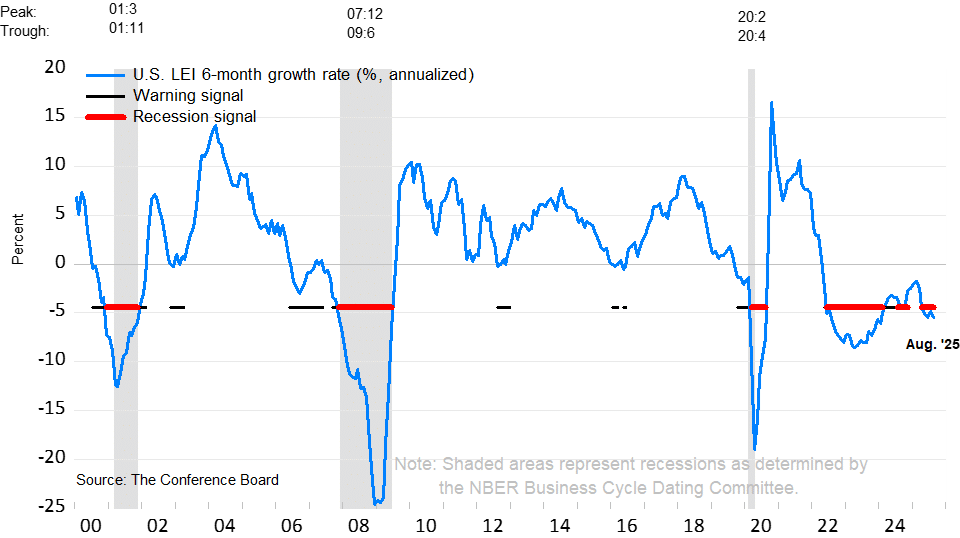

- Overall, the economic outlook, as measured by the Conference Board’s Leading Indicators, has now declined for 17 consecutive months.

- In this phase, the most successful investors remain fully invested, but rotate towards more liquid positions.

... where the second phase shows real signs of danger, where in ...

In phase two, forward guidance begins to soften or companies start issuing downgrades.

- We do not yet see this among companies.

- However, credit quality among private borrowers continues to deteriorate, prompting warnings from JP Morgan’s CEO Jamie Dimon in October about significant risk signals.

- Delinquent student debt is e.g. rising sharply: of the 45 million Americans with federal student loans, one in four is either in default or delinquent for more than 90 days.

- Short-term credit such as credit cards and auto loans is also increasing rapidly, recently leading to the collapse of auto finance companies including Tricolor Holdings and First Brands Group.

... the third phase, credit tightens

In phase three, credit tightens gradually and consumers become more cautious.

- There are no strong signs of this yet, but Jamie Dimon’s recent statements may serve as an early warning hereof.

- A further signal may be seen in Reverse Repos, where banks for the first time since Covid no longer hold large uninvested liquidity reserves.

- One of the most important indicators of overall tight liquidity remains Interest Rate Swaps (IRS), which are still relatively calm.

- IRS contracts are a major pipeline for global financial markets, both equities and debt. They are highly leveraged derivatives, settled only on the difference between parties. Sudden or significant interest rate discrepancies could leave one party under-hedged, potentially triggered by, for example, US tariff policies that may raise domestic inflation, eventually affecting global inflation.

- While the total global market cap is around $130 trillion for equities and $270 trillion for global debt, the IRS market totals $600 trillion.

- Such volumes are only possible due to deep trust among international investors. However, this trust has eroded in recent years as geopolitical interests increasingly translate into actions (e.g., the Ukraine war and tensions around Taiwan). This has led even long-term oriented central banks to increase their gold reserves; for the first time since 1996, these now exceed their holdings of US Treasuries..

In phase four, the labour market softens rapidly and broadly and credit issuance contracts sharply. By the time everyone realises what is happening, the market has already priced in the damage.

"Crises take longer to arrive than you think, but when they come, they happen faster than you can imagine." — Rüdiger Dornbusch

Are AI Equities Thus In a Bubble?

They are approaching that point. For now, however, AI stocks are less speculatively valued than dot-com stocks were in 1999. Moreover, in many ways they are also less speculatively priced than the broader market. Their growth potential remains substantial and diversified, which is why the risk of a major collapse in the near term is currently low. Nevertheless, they remain highly sensitive to continued financing, energy availability, and the ongoing supply of chips. Fundamentally, AI growth depends on a stable underlying economy.

By contrast, the broader market is in many ways more speculatively valued than AI. There is therefore a real risk of a larger systemic reaction if either economic growth or liquidity balance weakens.

Such a reaction could also arise internally, because US economic structures tend to push in that direction. A significant portion of the American population remains highly sensitive to further declines in real wages, as many lack sufficient financial reserves. This is happening at a time when the Federal Reserve has become more cautious about intervening with liquidity stimuli or interest rate cuts, due to inflation risks. At the same time, the central bank is under political pressure to reduce its influence in favour of a “free banking” system. In such a scenario, money creation could shift to private stablecoin issuers. This introduces new market dynamics, which could quickly accelerate an emerging loss of confidence.

One of the greatest biases in collective market psychology has always been the belief that “this time it’s different.” It has now been over 17 years since the last major financial crisis. This means that decision-makers are largely new among a very large segment of investors. Their actions are likely to follow the same patterns as their predecessors did before the last crisis. Lessons are often learned only by those who make the mistakes. Debt leverage, for example, is historically high, and few investors have a full overview of their systemic exposures.

"History doesn’t repeat itself, but it often rhymes." - Mark Twain