The US after NATO was unthinkable just a few months ago. Trump has however (re)launched a massive transformation agenda in the U.S., akin to the restructuring and turnaround of a deeply distressed company or country, e.g. Argentina.

The plan primarily assumes that the U.S. remains the world's sole superpower, ensuring the security of supply chains and the financial system. Trump believes the best way to achieve this is by using foreign policy to remind both allies and rivals of America's superpower status. In this process, he explores and tests all relationships to identify where momentum can be generated for broader negotiations, benefiting the U.S. in the short term.

In geopolitics, there are however no permanent friends, only permanent interests. The current decoupling from U.S. allies in Canada and the EU is, for now, to the advantage, and surprise, of Russia and China. In the long run, however, there is reason to believe that Trump's major trade confrontation will be with China. First, though, he must secure new supply chains, as China's global dominance in raw materials could cripple the U.S. economy.

Political decisions set the framework for economic development. But politics also reflects economic problems. Therefore, it is worth first outlining the current state of the U.S. economy.

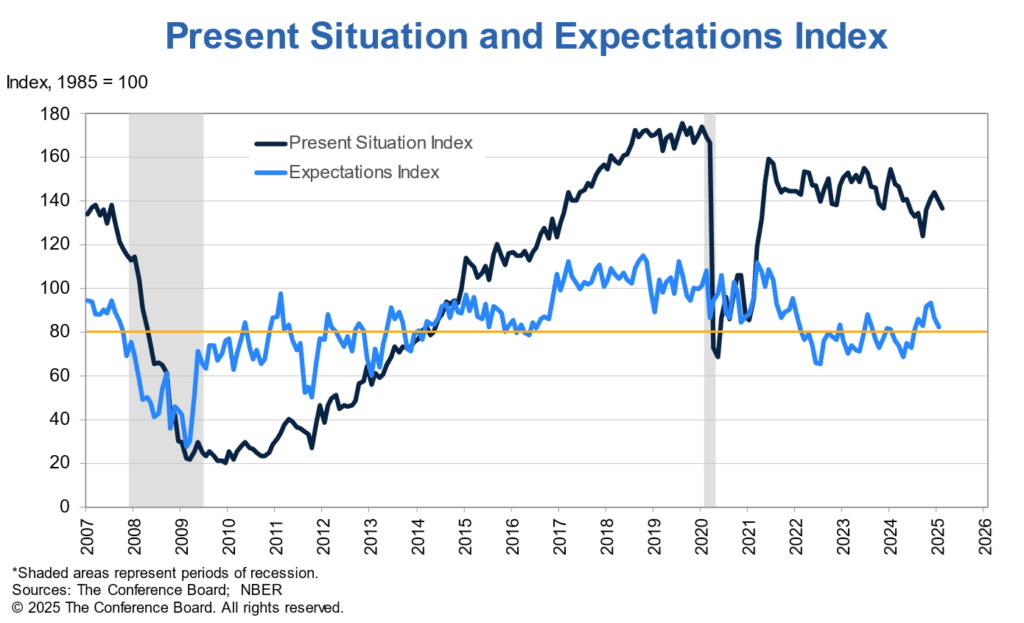

American economy is driven by private consumption

Economic growth is showing a declining trend. This is more dangerous than usual because U.S. debt is extremely high, and Trump's economic plan relies on sustained high growth.

Two-thirds of U.S. economic growth (GDP) is driven by private consumption. Therefore, consumer expectations are one of the most important barometers of the U.S. economy. These expectations are falling despite Trump's optimism, while many inflation indicators are rising. As a result, U.S. economic risk is currently increasing, perhaps even to the extent that a recession could emerge by the end of 2025.

Inflation is thus a particular risk, ...

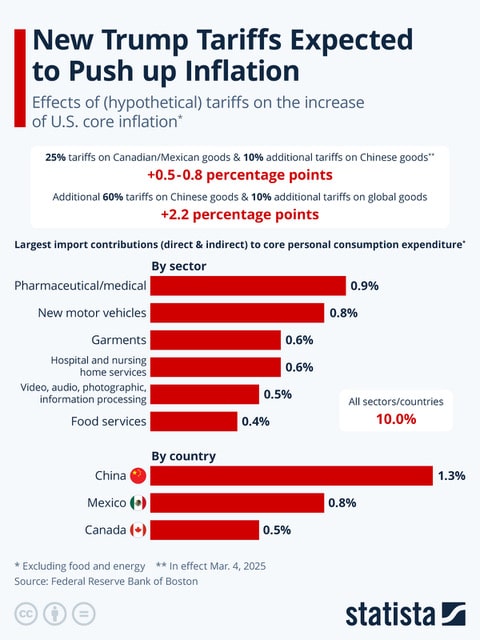

For many consumers, the recession is already a reality, as rising inflation erodes their purchasing power, i.e., real income. Rising inflation particularly affects low-wage earners, who spend the largest portion of their income and therefore have the least financial flexibility. Moreover, inflation prospects inflation prospects are now significantly worsened by Trump’s tariff war, which he has initiated against all countries, even though most tariff increases have since been suspended.

- A tariff is a duty that is passed on to the price of a good. It is therefore paid by the consumer, not the exporter.

- In theory, this makes competing American goods more competitive within the U.S. However, in many cases, the U.S. does not produce the goods subject to tariffs. The U.S. also often lacks the industrial capacity or supply chains to begin doing so. Such developments take many years to establish.

- The MAGA faction in the U.S. believes that tariffs will force exporters to lower their prices for the U.S. market. However, this argument is self-contradictory. In practice, it would require the U.S. to be a so-called monopsonist, meaning it would have such control over all imports that foreign suppliers would comply with U.S. price dictates. But if that were the case, tariffs would not be necessary—U.S. importers could simply enforce lower prices regardless.

- Furthermore, at best, tariffs can either protect domestic U.S. production or generate tariff revenues; not both at the same time. If tariff revenues are high, it means that American businesses continue to import large quantities, indicating a lack of domestic production.

- According to calculations from PIIE, the typical American household will see a decline in purchasing power (real income) of $2,600 per year. The lower the income, the more this will be felt.

- These calculations are supported by the fact that the number of auto loans in the U.S. that are in delinquency is now at an all-time high.

- According to calculations by the U.S. Federal Reserve in early February, the tariff increases Trump has already implemented will raise U.S. core inflation by between 0.5 and 0.8 percentage points, pushing inflation to between 3.6% and 3.9%.

... and Trumps plan also requires monetary stimuli, ...

This creates a new problem for Trump’s economic policy because when inflation is this high, it prevents sustained monetary policy stimulus.

- The Fed has two main objectives (Dual Mandate): ensuring price stability and promoting maximum employment. The ECB, for example, does not have the latter objective.

- According to the Fed’s experience and economic understanding, these goals can only be achieved in that order and priority. Therefore, the Fed refrains from monetary stimulus when inflation exceeds a range of roughly 2%, at least until financial stability is at risk.

- In contrast, Trump’s economic policy depends on the Fed acting as a financier by both lowering interest rates and expanding the money supply. This is because the federal deficit is set to increase further in the coming years.

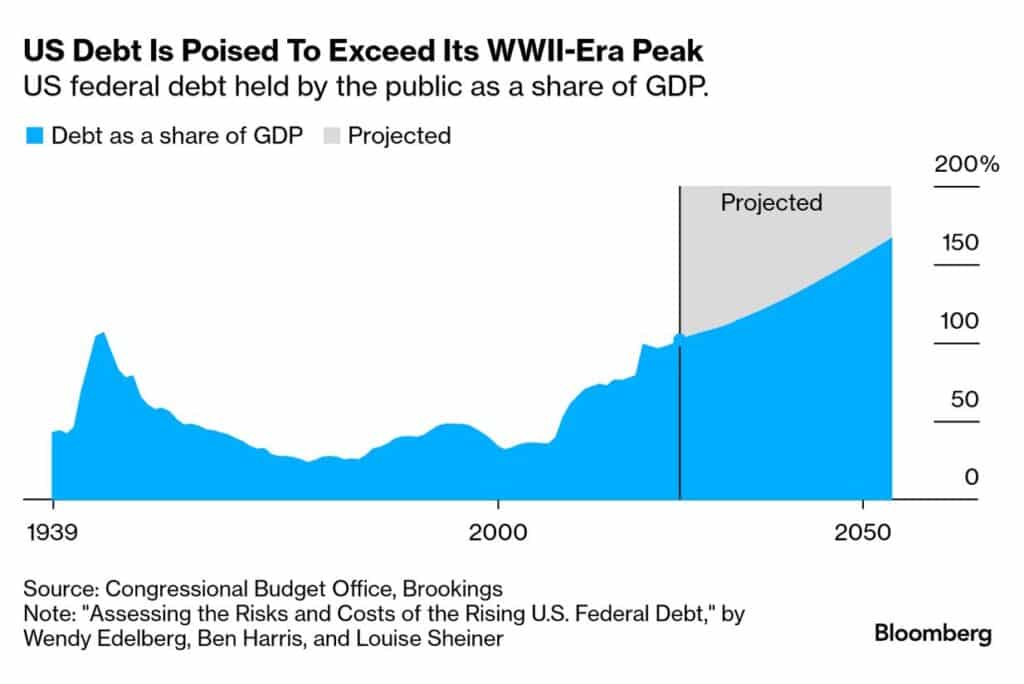

- Firstly, the U.S. national debt currently stands at a very high 123% of GDP. As a result, high interest rates lead to substantial interest expenses for the government; in 2024, interest payments accounted for one-sixth of total federal spending, amounting to $1.1 trillion out of $6.7 trillion. By comparison, the U.S. defense budget in 2024 was $886 billion.

- Even the most creative accounting cannot deliver savings of that magnitude, not even Elon Musk’s DOGE. Realistically, it is unlikely that more than $200 billion could be cut, even if the U.S. completely shut down its foreign aid programs to developing countries.

- Tariffs cannot close the gap either for the U.S. economy is relatively closed. According to PIIE calculations, tariffs would thus need to exceed 80% on ALL imports to cover the shortfall. According to estimates from the Boston Fed, this would push inflation up by approximately 5 percentage points.

- Furthermore, a key pillar of Trump’s economic policy has been to extend the tax cuts he introduced in 2017. Combined with other campaign promises, this would more than double the U.S. budget deficit over the next decade.

- It is also crucial to remember that the primary reason U.S. GDP growth has outpaced that of the EU over the past 20 years is that the U.S. has taken on far more debt.This high growth rate is NOT a reflection of significantly higher productivity or efficiency. Instead, like all debt-driven expansions, it means the government has pulled forward future economic growth opportunities.

... with which the Fed has very poor experiences

This is why it is critical for Trump’s economic policy that the Fed expands the money supply, that is, that it assumes the role of financier. For this reason, Trump wants influence over monetary policy..

- A larger money supply (either from monetary expansion or foreign capital inflows, i.e., FDI) is necessary to match the demand for money, which, in turn, is necessary to maintain financial stability.

- Trump is already preparing for the risk that the Fed will reject this role by publicly blaming Powell as the cause for the current inflation.

- So far, however, the Fed’s monetary policy committee, FOMC, has stuck to the hard-earned lessons on inflation that the central bank learned during the COVID era. At that time, the Fed assumed the role of financier for the U.S. government’s massive COVID stimulus packages.

- Those stimulus programs triggered a surge in inflation, which forced the Fed to hike interest rates—making the Fed technically insolvent due to massive bond losses on its balance sheet . The Fed does not want to end up in that situation again, as it would then have to ask the U.S. president for guarantees or capital injections.

This combination increases the risk for the US economy markedly

Although high U.S. debt levels are a concern, they are unlikely to trigger a debt crisis—at least “so long as the US retains its strong institutions and a fiscal trajectory that isn’t vastly worse than the one currently projected”.

- However, if a recession hits, both Trump and the Fed will face intense pressure—because more than a third of Americans lack the financial flexibility to withstand a real income decline of $2,600 per year.

- The rule of law is crucial for maintaining fiduciary trust, which in turn is essential for the U.S. dollar to remain the world’s preferred reserve currency. This "exorbitant privilege" is what defines a superpower from a financial perspective.

- Trump has repeatedly signaled how important he considers the U.S. dollar’s position—for example, by threatening 100% tariffs on countries that consider moving away from the USD.

- But this privilege is also essential for attracting foreign capital. This is the core of the America First Investment Policy (AFIP), which aims to "make the United States the world’s greatest destination for investment dollars, to the benefit of all of us."

- Saudi Arabia recently signaled in early March that it is considering allocating up to $1 trillion for investments in AI and quantum technology in the U.S. over the next 4-5 years. AFIP is thus meant to create a stabilizing floor for the U.S. financial system.

- For the rest of the world, however, the most important signal from AFIP is that Trump is reaffirming the U.S.’s commitment to the global financial system and the rule of law. After all, investors only commit capital if they have reason to believe they will get their money back one day.

To be continued in the next blog post