The U.S. megabanks are betting significantly on stablecoins, which promise a technologically efficient financial infrastructure.

On April 30, the U.S. Treasury Borrowing Advisory Committee (TBAC) gave a presentation on Digital Money. The focus was on stablecoins, which TBAC sees as having a major future.

Stablecoins as Digital Money Offer Scalability and Price Stability

Stablecoins are currently an attractive pathway for digital currencies because they are typically scalable while maintaining price stability.

Scalability means they avoid the Achilles’ heel of most cryptocurrencies: the limited number of transactions per second. For example, Bitcoin is currently capped at 5–7 transactions per second on Layer 1. In comparison, Visa can handle 24,000 transactions per second. While there are theoretical solutions for Bitcoin (such as the Lightning Network), they remain largely unproven in practice.

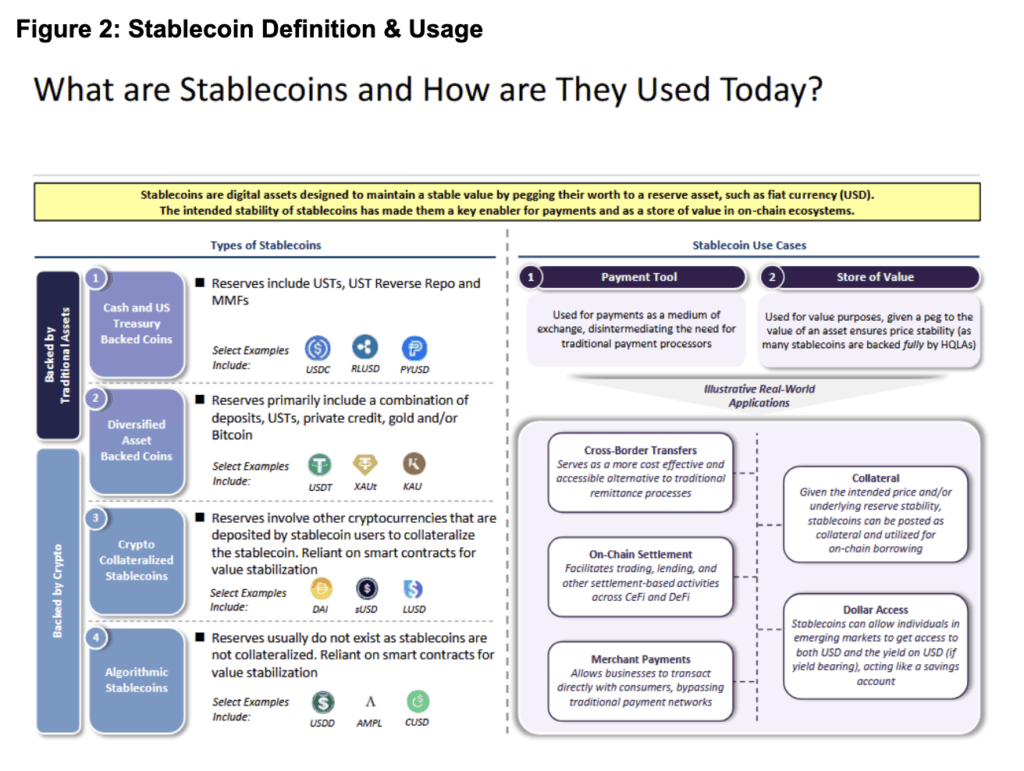

Price stability from stablecoins comes from being pegged to an existing fiat currency, usually the U.S. dollar. Their nominal value is often based on a 1:1 convertibility with USD, meaning stablecoins are essentially just a digital version of the dollar. The issuer typically backs this with a portfolio of U.S. cash, short-term Treasury bonds, repos, and other ultra-liquid and value-stable assets.

Among the best-known stablecoins today are Tether (USDT) and USD Coin (USDC). They are widely used in decentralized finance (DeFi) and for cross-border payments. Their key advantage is compatibility with blockchain networks, which makes transactions significantly faster and cheaper than through the traditional banking system.

Regulatory Gaps Remain Around Underlying Assets

More than 80% of the assets backing Tether are, according to its issuer Bitfinex, cash and other short-term deposits. The remaining 20% are higher-risk assets, such as equities. However, some other stablecoins are backed by significantly riskier assets—see the chart at the bottom of the page.

A general problem with current stablecoins is the lack of uniform standards for the underlying collateral (i.e., counterparty risk). Many existing stablecoin issuers are domiciled in regulatory havens and maintain their primary banking relationships in places like the Bahamas, as is the case with Bitfinex. They are also often not subject to full audits, but instead publish regular "attestations" showing their reserves.

As a result, there has been growing criticism of stablecoin issuers in recent years, notably from the U.S. Commodity Futures Trading Commission (CFTC). For example, a CFTC investigation in 2021 revealed that Tether had repeatedly failed to fully back USDT with actual U.S. dollars.

The absence of oversight and clear jurisdiction also means that stablecoins could, in theory, be highly speculative and leveraged—backed only by equities, for instance. That would constitute a potential pyramid scheme, where convertibility might vanish if the value of those equities drops.

U.S. Megabanks Are Now Heavily Investing in Stablecoins

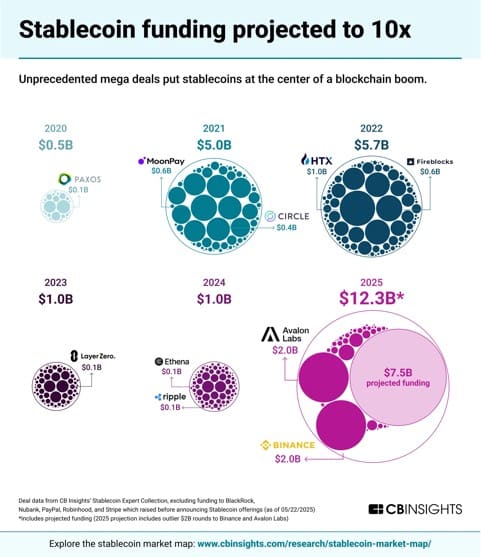

Despite these issues, the technological advantages of stablecoins are so compelling that nearly all major U.S. banks are now developing their own stablecoin units. Stablecoins are moving into the financial mainstream—where crypto failed to gain traction in 2021. IPOs related to stablecoins are expected to grow tenfold in 2025 compared to 2024.

There are multiple reasons for the recent surge, but most notably, major credit card providers like Visa and Mastercard, as well as large banks like JPMorgan, have now upgraded their systems to handle stablecoin transactions. They are also preparing to issue their own stablecoins.

However, stablecoins issued by megabanks and credit card companies will likely fall under stricter regulatory frameworks and be released in a more controlled format compared to USDT and USDC. These bank-issued digital currencies must comply with broader financial regulations governing securities and banking, which means they will be subject to formal supervision.

Most of these bank-backed "stablecoins" will likely be tokenized deposits or digital money, rather than freely circulating stablecoins on public blockchains like Tether.

JPMorgan Has Been Especially Active in This Space

Over the past several years, megabanks such as JPMorgan, Citi, and BNY Mellon have been developing token-based systems. These systems resemble stablecoins but operate with known counterparties and carry low regulatory risk. The focus has been on gaining experience with high-efficiency payment systems and intraday settlement.

Since 2020, JPMorgan has used its own JPM Coin for internal and institutional transactions. JPM Coin is not a public stablecoin but functions as a digital dollar on the bank’s private blockchain platform, Onyx. The bank is also actively working to tokenize traditional assets like Treasury bonds, deposits, and commercial paper. JPM Coin can be used in repo transactions, intraday liquidity operations, and international payments.

To support its stablecoin infrastructure, JPMorgan has participated in several pilot programs with central banks in recent years, including the Monetary Authority of Singapore (MAS) and Project Guardian.

However, the Transition to Stablecoins Could Have Deep and Political Consequences (See next blog post.)