Since its launch 10 years ago, Chinas Belt and Road Initiative (BRI) has become the biggest lender to development countries. The investments in these often fragile economies gave hope for economic upturn. Many countries however overestimated the economic effects from the BRI projects, and China was a very risk willing lender.

Today more than half the BRI lending countries are in distress and many are in debt spirals. Rather than writing off this debt, China typically offers rolling it or sale-and-lease back.

This has led USA to accuse China for "debt trap diplomacy", i.e. using distressed countries as leverage for their geopolitical policies.

What is the future for BRI and the BRI countries? Can problems here push too hard on Chinas fragile financial system? Is investing in developing countries a new geopolitical crank shaft?

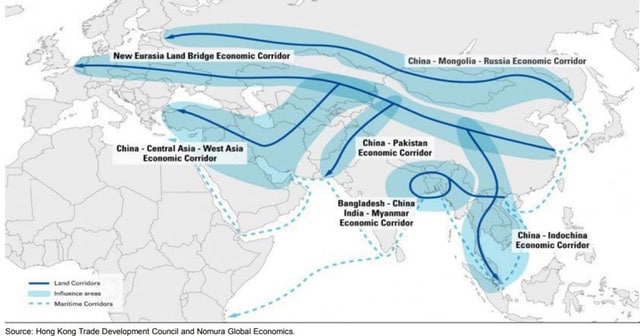

BRI is meant to remake China as "the Kingdom in the Middle", ...

When the chok from the financial crisis hit american and european consumers in 2008, it triggered a drop in non-essential consumption. This hit Chinas export driven economy abrupt and hard. Growth in Chinas industrial export e.g. dropped from +20% in Q3 2008 to -20% half a year later, cf. OECD (2011). The economy wasn't prepared to absorb such a massive chok, and it thus led to sudden mass unemployment and vacant factory capacity of between 30% and 80%, depending on sector, cf. Kawai (2012).

The chok led to the most remarkable rescue plan following the financial crisis: Chinas massive investment stimulus. This has today led to large structural over capacities on transport infrastructure and on properties, cf. Scharling (2023).

In China the government saw the financial crisis as yet another historical lesson on the need to reduce its dependency on others. Other countries should depend equally on Chinas economy as a supplier of essential goods as well as a lender .....

Read the full article from Finans/Invest (6/2023) below, or read on Finansforeningens web page