Climate economy depends a.o. on the supply chains for climate metals. The following is an extract from a paper, from the summer of 2023:

IPCC’s final AR6 report from March 2023 concluded, that global warming is caused by humans in particular from our energy production. This has increased the CO2 level in the atmosphere to more than 418 ppm, far above the ”safe limit” of 350 ppm. IPCC therefore concludes, that drastic and immediate changes must happen to avoid everlasting climate changes to the earth.

Climate transition investments are too small

Even though climate change investments are increasing they are still far from what is necessary to achieve the COP21 target. In 2023 renewable energy sources e.g. increased by 18% to 500 GW in total for wind, solar, nuclear and geothermic energy production plus energy storage. NetZero however requires an annual increase in this capacity of +1,4 TW before the end of the decade, i.e. a tripling to today.

Climate change investments are thus fundamentally too slow. In May 2023 World Meteorological Organisation (WMO) under the UN announced that the chance of reaching the COP21-target was only at 34%. In the 2022 that estimate was 52%. The former head of UNFCCC, Chistiana Figueres, believes that there is a lack of commercially viable solutions for at least the next 5 to 7 years. Countries not only invest too little, but many technologies also still need to be developed.

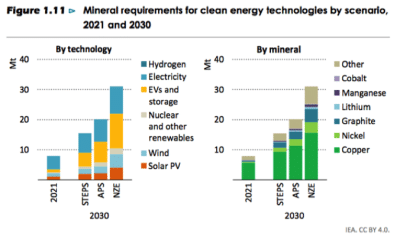

Climate change requires specific metals

Manufacturers of climate technologies therefore mean that we are pushing a snow ball of climate change decisions ahead of us. They are therefore ramping up their manufacturing capacities, in particular for solar panels and batteries.

There is however a risk that they will never be able to match the supply. Batteries e.g. require lithium and nickel, and transmission of electricity requires cupper. According to a study by MIT in 2023 there is still a natural abundance of the necessary climate metals. We however lack the mining capacities to extract them. Furthermore many of these are in countries that are geopolitically at edge with the developed world. That is the countries, who face the biggest climate change investments.

Copper

Copper is the best metal for conducting electricity, after the commercially inviable silver. It is therefore an achilles heal for the electrification, central to climate change investments.

- An EV (electric vehicle) uses 53 kg. of copper on average, solar panels use 2.8 tonnes copper per MW capacity and offshore wind 8 tonnes per MW. Climate change investments furthermore rely on significantly increased transmission and distribution capacity, i.e. high voltage copper wires.

- Global consumption of copper is therefore expected to double between 2020 and 2030, and to triple before 2040.

- According to the IEA from 2030 there will be an annual demand of more than 35 mio. tonnes, but the maximum extraction capacity including planned mines will only amount to 30 mio. tonnes. This produces a deficit of 15% already in 5-6 years.

- A new coppermine normally takes around 10 years to plan and construct, incl. infrastructure to the mine etc.

- New mines are therefore not commercially viable unless copper prices exceed app. 15,000 USD/ton. The current price is around 8,000 USD/ton.

- Therefore, the big mining companies such as BHP, Rio Tinto, Newmont and Glencore are currently active in acquiring smaller mining companies as well as increasing extraction from existing mines.

Nickel

Nickel is today predominantly used in rust free steel (70%) but also as anode material in batteries (together with manganese and cobalt). Wood Mackenzie expects that the majority of nickel usage by 2040 will be in batteries.

- A Tesla battery of 100 kWh contains e.g. 70 kg. of nickel.

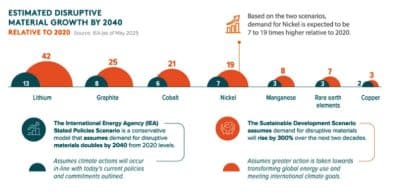

- Global consumption is app. 7 mio. tonnes a year. This is expected to multiply by between 7 and 19 times from 2020 to 2040.

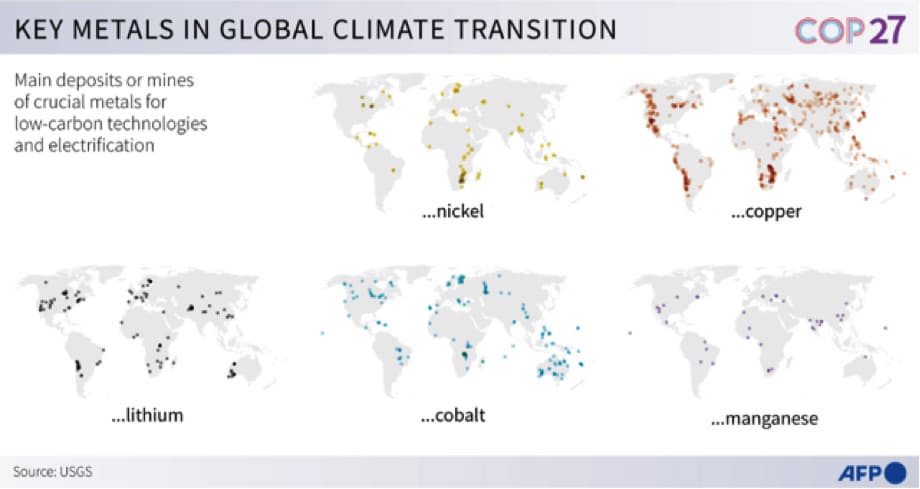

- There are plenty of natural nickel occurrences, and the constructing time for nickel mines typically take half as long as with copper mines. Indonesia has e.g. multiplied its mining capacity by factor 5 in under 5 years. It is today the globally far biggest mining country with a capacity 7 times as big as number 3, Russia.

- But it is the russian company Nornickel, that together with Brazilian Vale account for more than half of the global market. This also explains why the price of nickel increased by 250% in 2 days following Russias invasion in Ukraine in 2022. It also explains why the price has dropped since Lula took over presidency for Brazil from Bolsonaro in January 2023.

Lithium

Lithium is the most essential metal for electric batteries today and for the next 5-10 years. After this other minerals such as Vanadium or Sodium may assume a bigger role.

- To reach the COP21 targets, lithium consumption will have to multiply by factor 42 to today.

- Lithium has plentiful of natural abundance, e.g. in sea water. But in a commercially viable and concentrated form, it is primarily found in the "lithium triangle" (Bolivia, Argentina and Chile) as well as in Australia, USA and China.

- Australia is today the biggest miner of raw lithium followed by Chile and China. Globally, it is however mined in many locations including Germany and Sweden (Northvolt).

- But the total lithium mining must increase by factor 20-40 before 2040. This is VERY ambitious.

- IRENA e.g. sees that planned capacity is growing too slow.

- Furthermore China has more than 70% of the global processing capacity, i.e. from raw lithium to lithium carbonate.

- A lot therefore indicates that global lithium extraction will not be able to keep up with demand. In just a few years.

- Additionally, China can shut off global supply at discretion, whether to increase earnings or as a geopolitical tool.

Cobalt

There is also a scarcity for cobalt.

- Almost 70% of global cobalt extraction today takes place in DR Congo with massive ESG problems as a result. For extraction often takes place under horrible human and environmental conditions. Furthermore, the Governance dimension is particularly challenged.

- China is the biggest and almost sole lender to Congo (except for Russia) through ownership of the cobalt extraction rights and control of the mines. Wagner Group (now Africa Corps) is hired in to ensure "security" around the mines.

- Canada is currently increasing its cobalt extraction, but at about twice the price of DR Congo.

- A Tesla with a 100 kWh battery uses around 6 kg. cobalt. The target for 2030 is a total EV capacity of 10 TWh, equalling 600.000 tonnes of cobalt a year. For EV's alone.

- Today around 140.000 tonnes are extracted annually. DR Congo has a mining capacity of around 250.000 tonnes a year.

- Several manufacturers, including Tesla, work to reduce the usage of cobalt in favour of nickel. A complete phase out of cobalt however seems unlikely.

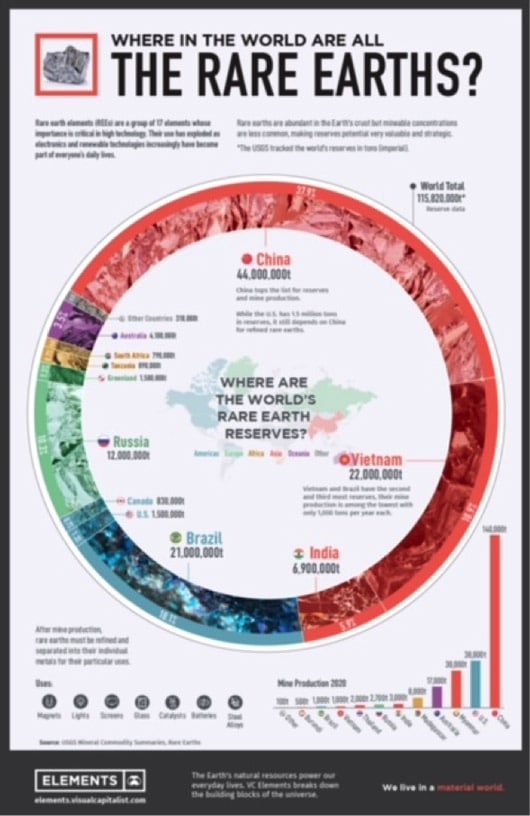

Rare earths

Rare earths are predominantly found in China but some of these are also extracted in Vietnam, Russia and Brazil. The term covers more than 17 basic chemical elements of the periodic system. Some of these are used in defence products such as the F35 aircraft.

- The 3 rarest of these are tellurium, a part of solar panels, and neodymium and dysprosium, that are part of the magnets and dynamos of wind mills.

- Tellurium is extracted via electrolysis during copper processing. This is particular the case in Chinese copper mines plus a little in Sweden. It is however processed and refined in Canada.

- Dysprosium and neodymium is extracted by pumping solvents in to the earth, the pump up the slag and then chemically filter this. This proces produces substantial environmental pollution and radioactivity.

- The minerals are only found in China plus a little but in Myanmar and in Laos.

- In 2019 China merged its mining companies for these rare earths in to two companies controlling a total of more than 85% of global extraction. There is however a substantial "black" market via Burmese entities, even though Burma is currently heavily sanctioned.

- Over the later years the Australian company Lynas has identified occurrences in Australia, but still less than a 10th of what is needed.

- There are also occurrences in California but with small capacities.

- Extraction of rare earths is limited to only 210 million USD a year. But they can still prove to be show stoppers for climate investments.

- The extraction corresponds to 0.06 percent of iron ore extraction, 4% of lithium extraction or 5% of cobalt extraction.

Gallium and Germanium

Gallium and Germanium are also key for some products.

- Germanium is a bi-product from zinc extraction. Gallium is a bi-product from the first phase of aluminum production (when bauxite is smelted in to aluminate).

- Today Germanium is a key component of industrial chips for radio communication, e.g. radar. It is also key for fiber optics, solar panels, satellites and for night-vision equipment.

- Last year China accounted for 68% of global production of Germanium, and roughly the same number for Gallium.

- But Chinas global dominance is primarily a result of China having the worlds biggest raw materials processing capacity. The metals are found and isolated almost everywhere, where zinc is extracted and where bauxite is smelted. But only a few countries process them.

- The day before Janet Yellen arrived in China on July 7, China announced an escalation of its trade war with the US. This time they prohibited the export of Gallium ang Germanium for reasons of "national security". It was seen as a quid-pro-quo response to the US embargo on advanced micro chips, with symbolic references to France and Germany.

- The export ban was first and foremost a symbolic demonstration of power. Since the spring of 2023 the US has sought alternative supply routes for Gallium. The NSA estimates that both metals can have full redundant setups before 2024.

- Chinas embargo should there be viewed as a general warning on rare earths.

Silicium

Finally, Silicium is extracted in many parts of the world.

- But for the use in advanced microchips, Silicium needs a purification of +99,999%.

- Only one mine in the world can produce so high a purity, the Spruce Pine mine in North Carolina.

- The mine already supplies 80% of the worlds high quality quartz (silicium).

- When TSMC’s factory thus opens in Nevada (delayed) in 2025, the US will have control over both resources AND processing for advanced electronics. No other country in the world will be able to match this.

Under-supply produces a climate economy risk

In periods of sustained and substantial undersupply, prices rise significantly unless politics prevent this. In most cases this equals China. The return on investment of global climate change investments can in other words be at risk if China decides to liberalise the mining companies. This would at the same time increase Chinas geopolitical influence substantially.

The US, EU (Critical Raw Materials Act) and the G7 are all aware of these bottle necks. At the G7 council in April 2023 it was decided to produce a plan for lithium mining worth more than 7.5 billion USD. But copper, cobalt and in particular rare earths require Chinas active participation. And silicium requires the good will of the US.

The effect of under supply can therefore significantly affect the price for climate change technologies. In most cases the effect will however be transient, because there are significant innovations underway. This particularly applies to energy storage, the biggest achilles heel of climate change investments.