The U.S. decoupling from NATO partners leaves a geopolitical power vacuum. This creates opportunities for China, Russia, and India, but especially for alliances such as BRICS+..

The decoupling increases China’s influence in Asia and particularly in African nations, as it raises doubts about the U.S.’s willingness to secure global maritime “freedom of navigation”, the foundation of its military superpower status. Furthermore, the decoupling provides China with a new and much-needed opportunity to avert a financial collapse.

For this reason, China has a vested interest in a form of pact with the EU, whose supply chains depend on China and which could assist China in securing investments in developing countries.

In geopolitics, there are however no permanent friends, only permanent interests.

A stable economy is important to China ...

Politics reflect economic challenges and shape the framework for economic development, at the same time. Although China is an autocracy, its internal stability and unity rests on public trust in the Communist Party’s (CCP) ability to manage the economy prudently (“the social contract”). This makes a stable economy crucial for the CCP’s grip on power. It is thus relevant to first outline the current state of China’s economy.

There are two narratives about China's economy, both of which are true:

- One describes an economy deeply dependent on exports, and at risk of collapse due to an extreme debt burden.

- The other highlights China's rising economic and technological power.

... because the enormous debt increases the sensitivity ...

At some point, one of these narratives will become dominant, but it is too early to determine which. This depends largely on external factors, such as the extent to which Trump decouples the U.S. from the rest of the world, The severity of U.S. trade wars and The level of global control the U.S. achieves over AI and chip development.

Most factors are therefore beyond the direct control of the CCP. However, the margin for error on internal factors is extremely narrow, given China’s current level of debt.

- China’s national debt is on par with the U.S. (123% of GDP) when combining local and central government debt. However, corporate debt is also exceptionally high, bringing China’s total debt to 312% of GDP.The majority of these companies have the state as a majority shareholder. This makes China’s debt highly systemic.

- Debt serves as a stimulus tool for future growth, but fundamentally, it also reflects a forward accrual of future spending capacity.

... towards a continuously high growth rate

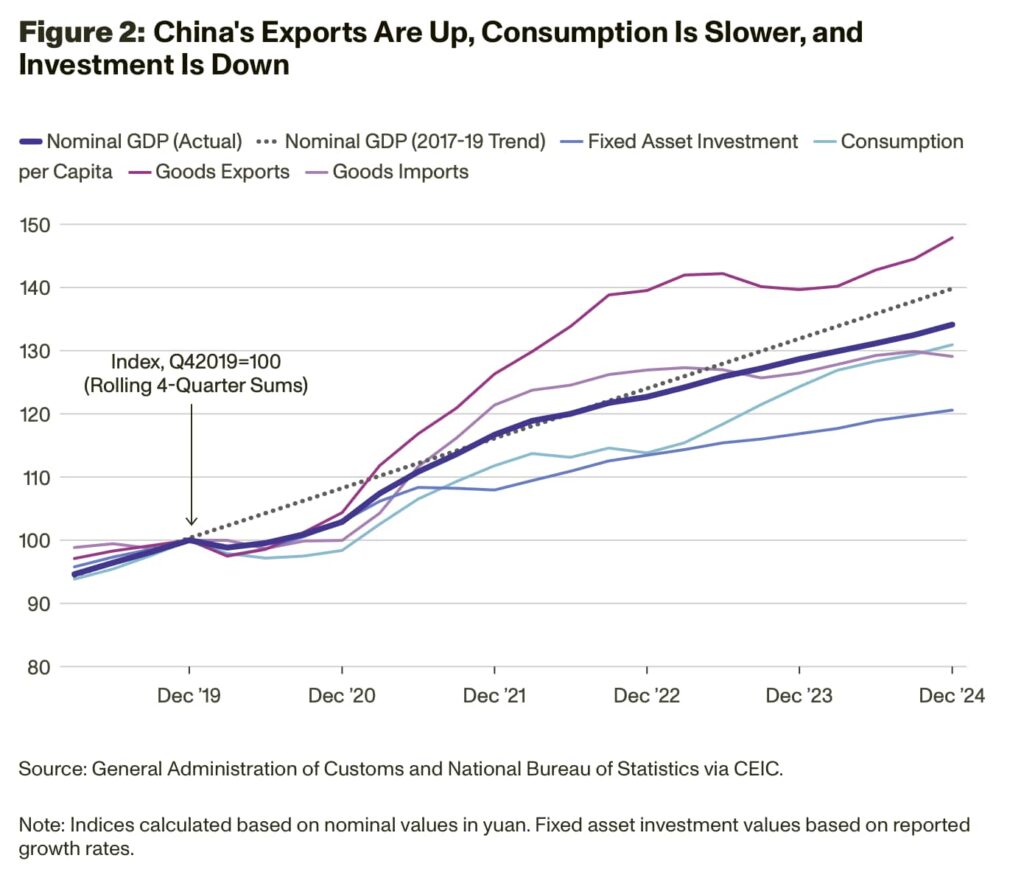

China’s economy depends on maintaining very high growth rate of at least 5%. Otherwise, a debt collapse could be triggered by factors such as rising interest rates, which can erode budgets and profits, further declines in private consumption, a decline in investment growth, a drop in exports og a decline in financial inflows, e.g. foreign direct investments (FDI).

Private consumption in China "only" amounts to a third of GDP, i.e. half the share as in the U.S. and EU. This is however something, the government can actively address.

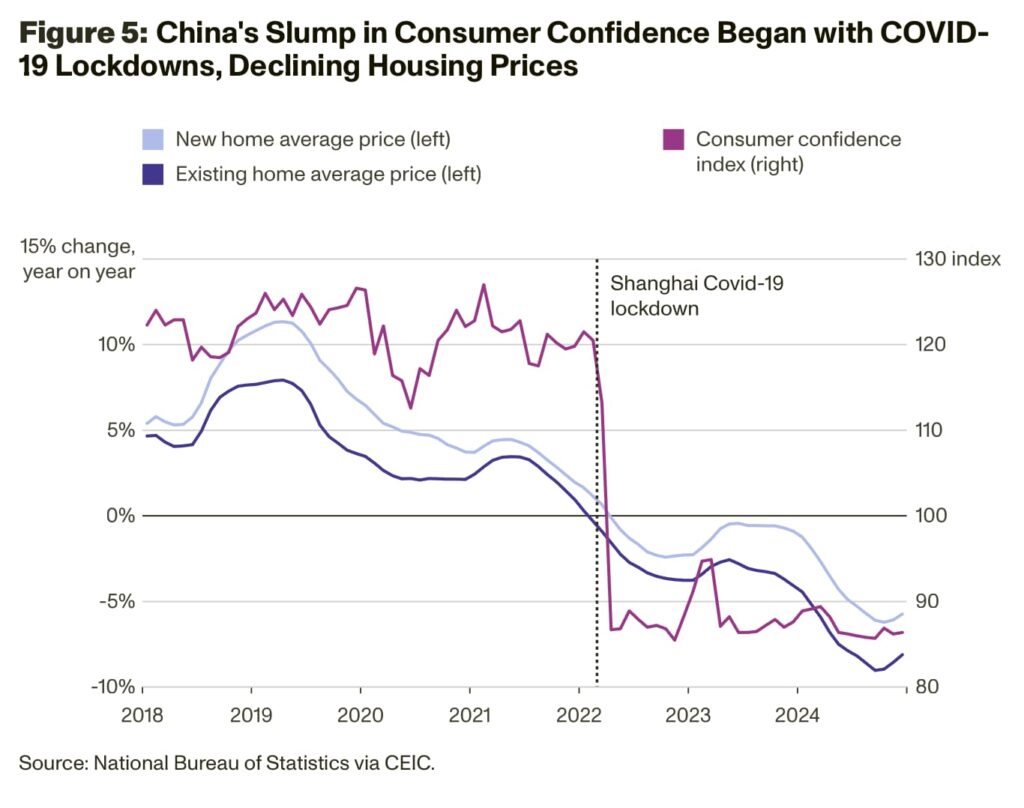

Optimism in private consumption is however under pressure ...

Faldet i forbrugeroptimismen blev udløst af Covid udbruddet og de massive og langvarige lockdowns. Men Covid udbruddet faldt også sammen med et tipping point for Kinas aldersdemografiske skævvridning oven på 36 år med et-barns politik. I de kommende år går stadig flere kinesere på pension ligesom fødselsraterne samtidig er kollapset. I 2024 blev der født mellem 1,1 og 1,2 barn per kvinde. Det er kun godt halvdelen af det niveau på 2,1, der er nødvendigt for et neutralt befolkningstal. Det har startet en depressiv privatforbrugsspiral. Regeringens stigende stimuli har endnu ikke har ændret retningen på det. Foreløbig har det “kun” evnet at slukke ildebrande, dvs. sikret finansiel stabilitet.

… fra en næsten “perfekt storm”

The longer the downward spiral lasts, the harder it becomes to break. Mass psychology takes time to shift, especially when demographics are rapidly tilting toward retirement and wealth decumulation.

This has impacted real estate, the primary investment and savings vehicle for the Chinese population, where prices continue to fall despite a collapse in construction activity (supply). The oversupply of housing relative to demand is up to 20%, and in some areas over 50%. It will take many years to restore equilibrium in the real estate market, and China’s strict immigration policies do not alleviate the problem.

However, depressed consumption and declining property prices have also led to zero inflation. In reality, China is on the brink of deflation, which represents its worst financial nightmare due to the extreme debt levels. Deflation could trigger what China itself calls the “Japanese Trap”, i.e. a scenario where real wages and asset values decline over multiple decades. China largely attributes Japan’s stagnation to the Plaza Accord, which the U.S. (under James Baker) forced through in 1985.

China's economy therefore needs positive news ...

China thus views Trump’s threats of a forced currency agreement (e.g. the draft “Mar-a-Lago Accord”) very seriously. It is also a key reason why China has pushed for a BRICS+ currency. If combined with a broader decoupling from the US led financial system, it would effectively neutralize the effect from a new Plaza Accord. Alternatively, it could set off a massive financial collapse in China, which could resurrect the specter of the “Century of Humiliation.”

This term is central to China’s modern self-perception and geopolitical agenda, referring to the period from the First Opium War (1842) to the founding of the People's Republic (1949), a time when China was forced to cede territories such as Outer Manchuria, Hong Kong, Macau, and Taiwan. The era culminated in Japan’s occupation of Manchuria from 1931 to 1945.

Because of this, China is determined to maintain high official growth figures. The methodology for calculating these figures is a state secret, and neither foreign analysts nor independent think tanks have been able to validate them.

- China’s late Premier Li Keqiang famously called GDP figures “man-made” and “unreliable” in 2007 (WikiLeaks, 2010).

- Independent institutions such as credit rating agencies, Rand Policy, Brookings, and Rhodium Group estimate that China’s actual GDP is overstatedby up to one-third when measured using Western methods (EU/US).

- This means China’s real debt ratio could exceed +400% of GDP. A debt collapse could thus be triggered by even minor interest rate hikes or by capital flight due to declining foreign direct investment (FDI).

China’s economy is thus at serious risk of collapse, especially if Europe also starts pulling back financially. After all, it was foreign capital flight that triggered the Asian financial crisis of 1997-98. This is why, over the past two years, China has ramped up international investment conferences. In March is was Boao Forum, China’s version of Davos.

... but it is important to remember, that China's economy has some tools ...

However, it is crucial to remember that China is an autocracy, has a systemic foundation under its economy, and is the world’s leading exporter of critical products. These factors extend the timeline until a potential debt collapse.

Autocracy allows the government to force through policies that democracies cannot. Moreover, Chinese consumers have historically been highly patriotic when the government has called upon them to be. For example, while exports are slowing, imports have remained neutral. In contrast, American and in part also European consumers and businesses lack this level of economic patriotism.

... like e.g. being globally and systemically connected ...

The systemic foundation of China's economy also stems from the Belt and Road Initiative (BRI). Through BRI, China has invested so heavily in developing countries that many are now financially dependent on Chinese funding and trade. Moreover, BRI loan agreements often come with political conditions, giving China the potential to exercise “debt-trap diplomacy” if necessary.

- China has signed over 200 BRI agreements with 150+ countries and 30 international organizations, funding $1.3 trillion in infrastructure projects. The total outstanding debt stands at nearly $1.1 trillion, and 80% of BRI loans have been issued to financially distressed nations.

- However, the debt-trap strategy only works as long as the U.S. and EU lack viable alternatives to BRI. The future of the West’s competing initiative, PGII, is under serious threat, due to Trump and Elon Musk’s dismantling of USAID.

- According to a 2024 AidData study most developing nations actually prefer to borrow from the U.S. and EU, but Western lenders have imposed stricter credit terms.

- The EU’s Global Gateway thus needs to redefine its strategy. China’s Foreign Minister Wang Yi has recently reached out to the EU to explore “coordination and cooperation” on infrastructure investments. For Europe has a long-term geopolitical nightmare from Africa's demographic explosion.

- In 1950, Europe’s population was twice the size of Africa’s—today, it is the opposite. By 2100, Africa’s population is projected to be six times larger than Europe’s.

- Unless Africa successfully develops its economies, for example, through infrastructure investments to mitigate the worst effects of climate change, Europe will likely face massive waves of African migration.

- If, however, Europe actively supports African economies, it could eventually create new markets for its agricultural products, partially replacing lost U.S. export opportunities. In the longer run, the same could apply to industrial products as well.

... and being technologically leading in ever more areas

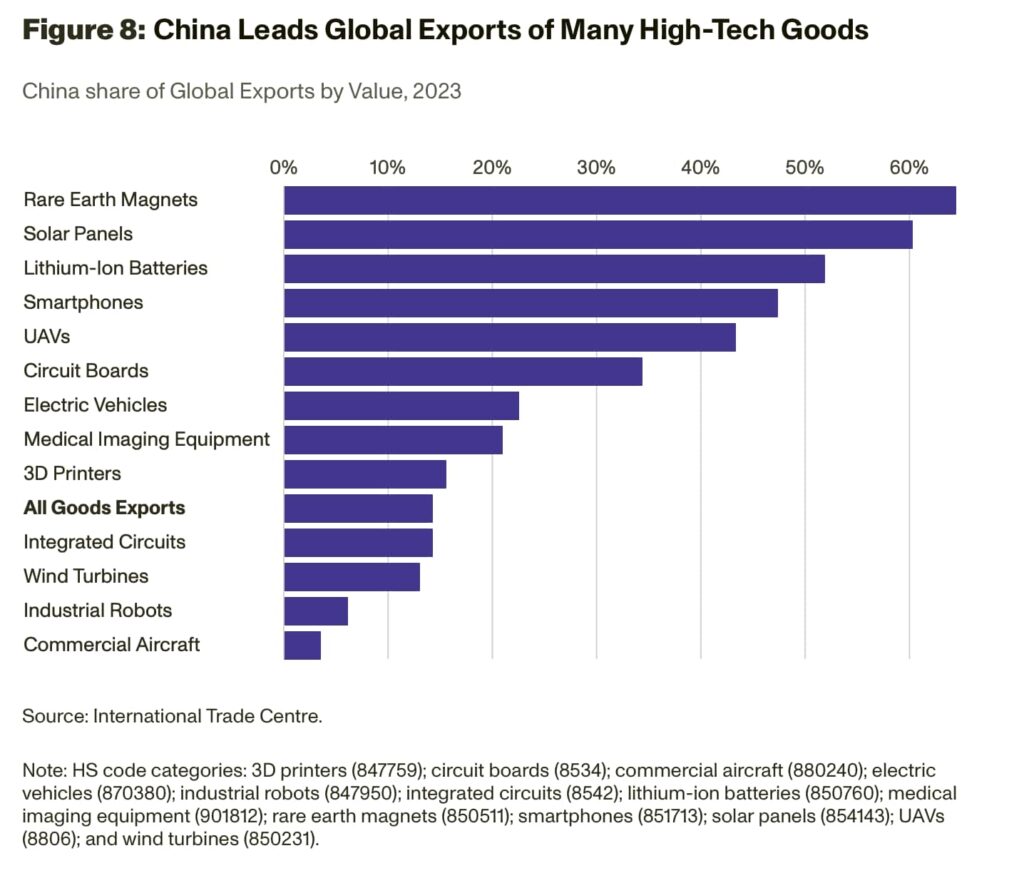

China is the world's leading exporter of many high-tech products and also holds the global lead in most key technologies of the future..

Although a trade war with the U.S. might dampen China’s exports, the growth potential in high-tech sectors thus remains significant. For a U.S. trade war to be effective, it would need to be prolonged and coordinated with several allied nations. Since Trump's inauguration, the latter is no longer a given. This is why China with relief views Trump’s threats to dissolve NATO, his public attempts to interfere in European democratic elections, and his ambitions to annex Canada and Greenland.

Additionally, China is the world's leading manufacturing country for a wide range of products, including ships. Finally, China holds a global leadership role in the extraction and/or processing of many critical raw materials, including those essential for climate transitions. For example, China controls around 80% of all graphite extraction and processes about 70% of it. Graphite is a crucial anode material for Li-Ion batteries, among others.

Today, China is better prepared for a trade war with the US

When Trump initiated his first trade war seven years ago, China was relatively unprepared. Today, China is acutely aware of its globally dominant role in supply chains. Shortly after Trump’s election, China illustrated this awareness by imposing a temporary export ban on gallium, germanium, antimony, and "superhard" metals in December 2024.

- A prolonged export ban on gallium and germanium could, for example, initially reduce U.S. GDP by $3.4 billion.In the long run, shortages of products containing gallium and germanium could amplify systemic effects in the U.S.

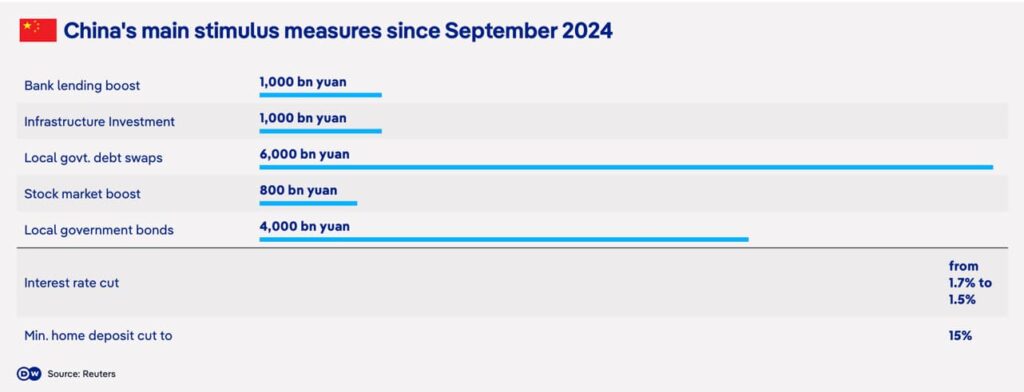

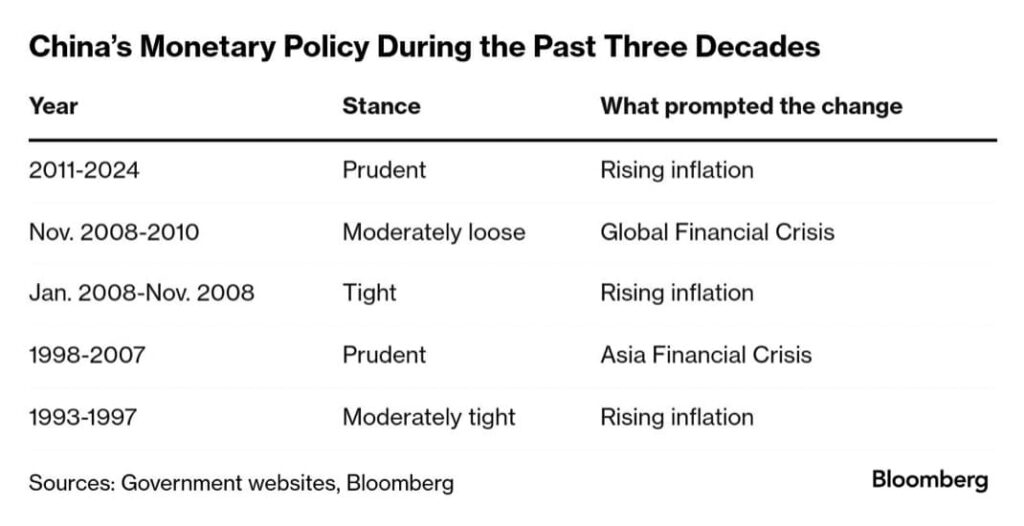

Samlet er både CCP og centralbanken PBoC dog nu blevet krystalklart bevidste omkring risikoen for økonomiens kollaps. Den stående komité har ophøjet privatforbruget til den øverste nationale prioritet og har bl.a. hævet landets gældsloft til mellem 4 og 5% fra de hidtidige 3%. PBoC fører samtidig en såkaldt “Moderately loose” pengepolitik. Det er på linje med den alvorligste tid under finanskrisen.

All in all China still has the potential to avoid a financial collapse, even if the U.S. launches a full-scale trade war against it. The U.S. decoupling from the EU presents a historic opportunity for China to establish cooperation agreements with the EU and African nations.