The alternatives to the Suez Canal can erode Egypts geopolitical "soft power". But only by up to one quarter of its capacity. Therefore, the major risk to Suez remains the Bab el-Mandeb entry to the Red Sea. This is the third blog post in the sequel of five on maritime bottlenecks.

Trade Between the EU and Southeast Asia Relies on Both the Malacca Strait and the Suez Canal

Alongside the Malacca Strait, the Suez Canal is a critical bottleneck for maritime trade between Europe and Southeast Asia. The natural alternative to the Suez Canal is the route around Cape Town. This detour however adds 10-12 days to the travel time. As a result, 10-12% of global trade passes through the Suez Canal annually. This includes up to 30% of global container ships.

Suez har givet Egypten stor “soft power”, …

Since Nasser’s nationalization of the Suez Canal in 1956, it has provided Egypt with considerable geopolitical leverage, including security guarantees from the U.S.The world witnessed the canal’s importance acutely during the Ever Given incident in March 2021. The container ship blocked the canal for six days. This delayed over 400 ships causing direct economic losses exceeding $1 billion.

The Suez’s geopolitical significance also extends fromits role as a hub for 16 undersea data cables, which facilitate about 17% of global internet traffic .

...But Its Importance Also Depends on Free Passage Through Bab el-Mandeb

To traverse the Suez Canal, ships must also pass through the Bab el-Mandeb Strait at the southern end of the Red Sea. This strait’s significance is underscored by Djibouti’s status as the world’s most militarized port. Djibouti hosts naval bases from France, the U.S., China, Japan, and Italy. Saudi Arabia and India are also planning bases nearby. The UAE operates a base in Eritrea, and finally Russia and Iran are pursuing naval facilities in Sudan.

Dén “soft power” er meget eftertragtet

Egypt’s dominance has spurred numerous attempts to create rival routes or redundancies for the Suez Canal. This trend has intensified in recent years.

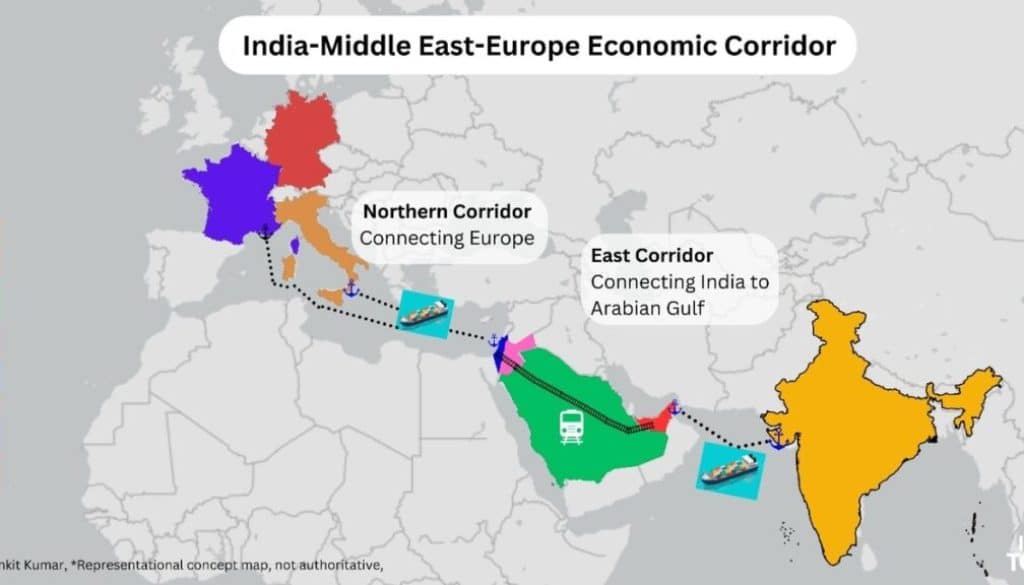

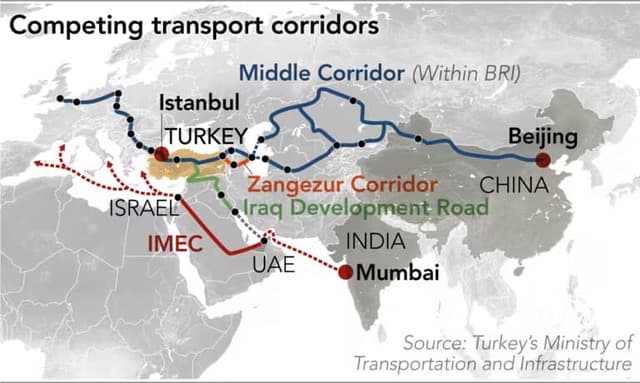

The first major competitor is the Western-Supported IMEC ...

The India-Middle East-Europe Economic Corridor IMEC) connects Mumbai, the Arabian Peninsula, Haifa in Israel, and ports in Greece and France. Initiated in September 2023, it

aims to challenge China’s Belt and Road Initiative (BRI) . MoU for the project was signed in September 2023 by India, the United States, the UAE, Saudi Arabia, France, Germany, Italy, and the EU. However, the project slowed down following the outbreak of the conflict between Israel and Hamas. Additionally, both Turkey and Egypt have protested against the project, as it bypasses their territories.

... which could notably alleviate the Strait of Hormuz

The project's capacity has not been finalized, but official statements suggest it could handle approximately 200 million tons of cargo annually, equivalent to one-sixth of the current traffic through the Suez Canal. IMEC could potentially expand to handle up to 500 million tons of cargo annually.

Furthermore, the project could alleviate pressure on the Strait of Hormuz, as IMEC includes pipelines for hydrogen transportation. Saudi Arabia is heavily investing in the production and export of green hydrogen as a future replacement for oil under its "Vision 2030."

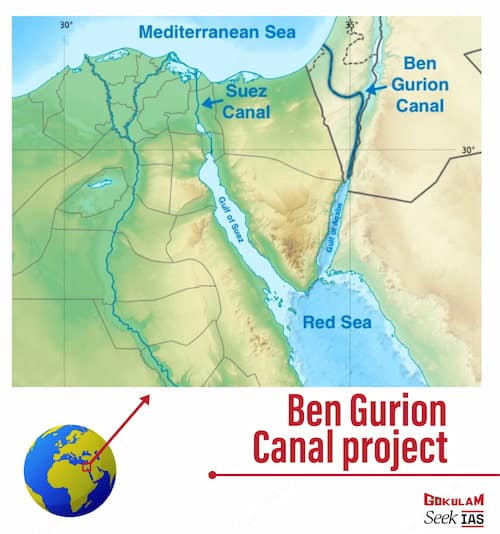

In practice, IMEC would replace Israel’s long-projected Ben Gurion Canal, as detailed below.

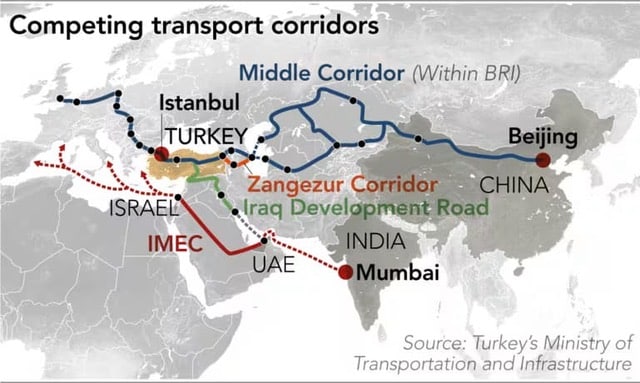

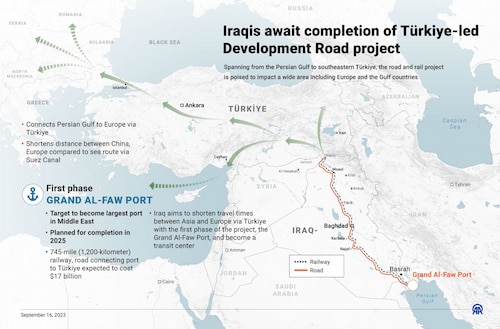

The next major project is the Turkish-supported IDR...

In April 2024, Turkish President Erdogan visited neighboring Iraq for the first state visit in 13 years. During the visit, the two nations signed 24 agreements as part of the Iraqi Development Road (IDR) project. IDR is a transport corridor that begins at a new deep-water port in the Persian Gulf, Grand Faw. It is combined with the extensive renovation of the 1,200-kilometer railway through Iraq. From there, Turkey is set to extend the railway connection to the Mediterranean.

The construction of Grand Faw Port is well underway, with planned capacity to rival Port Said in Egypt and Abu Dhabi in the UAE. In the long term, the project is expected to handle 40 million tons of cargo annually.

... which even seems to reconcile Turkey and Iraq’s relations...

Relations between Turkey and Iraq have been strained over the past 13 years due to Iraq’s recognition of the autonomous Kurdish region in the north. However, the project is so mutually beneficial that the agreements from April include Turkish guarantees for the flow of water from the Euphrates and Tigris rivers. These are critical lifelines for Iraq. The agreements furthermore included commitments from Iraq to take stronger action against the Kurdistan Workers' Party (PKK).

... and which attracts investments from the UAE and Qatar

Simultaneously, the UAE and Qatar signed agreements for both funding and use of the freight corridor. The biggest loser from IDR would be Iran, as the project positions Iraq as the new nexus of the region. Turkey’s involvement ensures that Erdogan’s geopolitical vision remains viable.

The final capacity of the project is still under review, but Iraq’s government believes the goal should be 100-150 million tons of cargo annually, roughly one-tenth of the Suez Canal’s capacity. The project has the potential to scale up to 200 million tons of cargo annually.

Since 2022, Russia has sought to significantly accelerate the INSTC…

Russia, Iran, and India have had plans to establish the International North-South Transport Corridor (INSTC) since 2002. However, the plans remained largely static until Russia's invasion of Ukraine in 2022. Since then, Russia’s trade with the EU has dropped to less than 10% of pre-2022 levels. As a result, Russia sees increasing geostrategic value in relieving its supply routes through the Danish Straits.

Consequently, Russia is modernizing its railway connections to Azerbaijan, while Iran’s upgrades are proceeding at a more moderate pace. Iran maintains a fundamental skepticism toward Russia.

… although the project will take decades to reach reasonable capacity

The long-term vision for INSTC is to make freight 30% cheaper and faster than the Suez route. However, this is a very long-term goal. By 2030, freight capacities are only expected to reach 20-30 million tons annually. By 2040, the port of Chabahar is expected to be modernized, increasing capacity to around 40 million tons annually. By 2050, the figure could rise to 50 million tons of freight per year, equivalent to approximately 4% of the volume currently transiting through the Suez Canal.

However, significant uncertainties surround the project, particularly regarding the ports of Chabahar and Bandar Abbas. The timeline could easily be extended by additional years or even decades. Particularly if instability in the Caucasus intensifies, such as in Georgia or between Armenia and Azerbaijan, potentially related to the Zangezur Corridor..

Russia’s oil exports will still need to be shipped from Primorsk and through the Danish Straits or via separate oil pipelines.

Thus, Suez is primarily challenged by capacity-relieving competitors, while the greatest risk remains Bab el-Mandeb

In total, projects are emerging that could potentially relieve up to one-quarter of Suez’s capacity. However, no more than that, and only within 20 years, provided there is geopolitical and domestic stability in all the countries involved.

As a result, shipping companies will continue to choose between sailing around Cape Town or through the Red Sea. The latter remains the more attractive option. It however depends on the continued availability of international war risk insurance, such as that provided by Lloyd’s, Gard, North P&I, and Standard Club.

See also the two previous and two subsequent blog posts in the sequel on maritime bottlenecks.