Alternatives to the Strait of Malacca can provide their hosts with geopolitical “Soft Power”. Fundamentally, they are however only large enough to serve as relief routes. Nevertheless, China is investing heavily in them. This is the second blog post in the sequel of five on Maritime Bottlenecks.

The Strait of Malacca: Nexus for south and east Asia's trade with the EU, India, and Africa

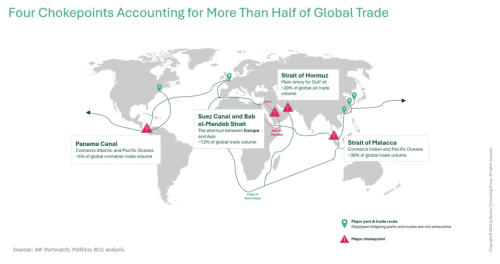

The Strait of Malacca, located between the Malay Peninsula and Sumatra, is the most critical juncture connecting the Indian Ocean with the South China Sea and the Pacific Ocean. It serves as a key trade corridor for nations such as China, Vietnam, the Philippines, and Japan in their commerce with the EU, India, Africa, and the Americas.

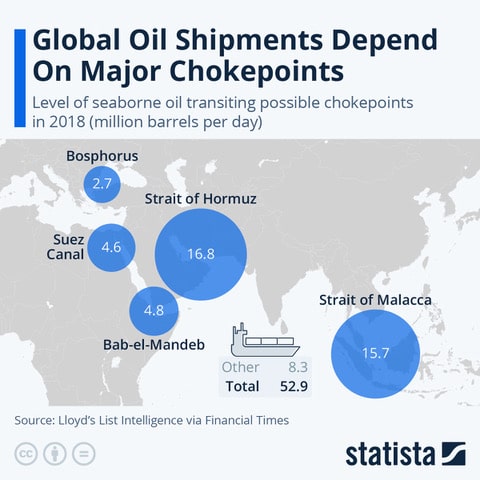

Every year, over 90,000 vessels navigate the mere 2.8-kilometer-wide strait. By comparison, 183,000 ships transit the English Channel, 20,000 pass through the Suez Canal, and 14,000 use the Panama Canal. The tonnage passing through Malacca amounts to roughly 3.5 billion tons, equivalent to 30% of all global trade. In monetary terms, this represents around USD 4.2 trillion.

China’s Critical Dependence on the Strait

As the world’s largest exporter via maritime routes, more than two-thirds of China’s trade passes through the Strait of Malacca. This includes exports of finished goods and, more critically, imports of raw materials and resources. Among these, two vital imports for China are food and energy. Notably, about 80% of China’s annual crude oil and LNG imports pass through the strait.

Strædet giver stor geopolitisk “soft power” …

The passage through the Strait of Malacca is primarily governed by the United Nations Convention on the Law of the Sea (UNCLOS) of 1982, which grants ships the right to continuous and unhindered transit. According to UNCLOS, the three coastal states—Malaysia, Indonesia, and Singapore—are obligated to ensure unimpeded and cost-free transit through the strait. However, the ports around the strait generate significant revenues from maritime activities.

Geopolitical Significance Enhanced by the South China Sea

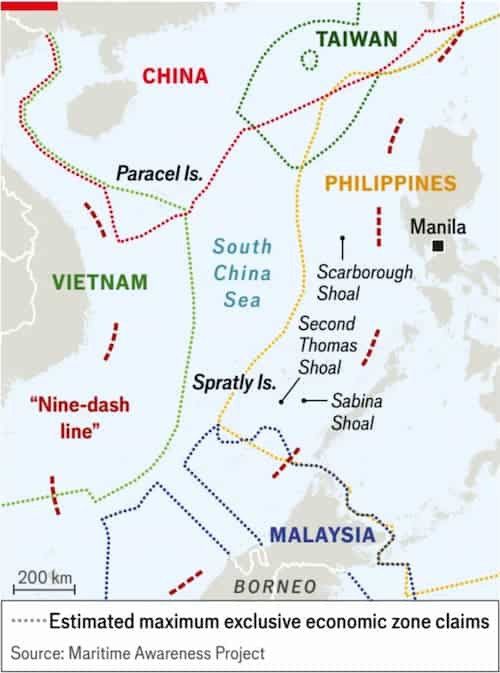

The geopolitical importance of the Strait of Malacca is amplified by overlapping territorial claims in the South China Sea. Escalating maritime conflicts in the region could easily disrupt civilian shipping, as opposing parties might block supply routes to their adversaries. Given that all major powers rely on the strait, it has long provided Singapore with significant geopolitical “soft power,” much to the concern and envy of other nations. These concerns have led to efforts to establish alternatives or supplements to the strait.

Thailand’s Persistent Efforts to Develop Alternatives

Since the 17th century, Thailand has sought to create an alternative to the strait, proposing a canal across the narrow Kra Isthmus, connecting the Andaman Sea and the Gulf of Thailand. In modern times, this idea has resurfaced repeatedly, particularly after World War II, during the 1970s oil crisis, and as China’s economy, and its dependence on the strait, grew.

In 2005, Thailand and China signed a Memorandum of Understanding to construct a canal through Kra. When China launched the Belt and Road Initiative (BRI) in 2013 , the project was among the first included under its umbrella. However, Thailand subsequently shelved the project, fearing it would exacerbate secessionist demands from its southern minorities, which have been growing since the 1940s.

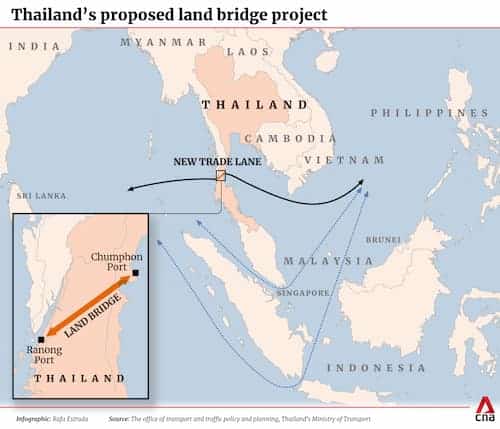

Thailand’s Land-Based Corridor

In March 2024, Thailand unveiled the Thailand Landbridge project, a USD 28 billion, 90-kilometer transport corridor across Kra. The corridor will include railways, pipelines, and highways, and is considered less sensitive to secessionist risks.

Thailand is currently seeking funding, with China and the UAE as potential investors. Construction is expected to begin in 2026, with partial operation anticipated by 2030. Once fully operational, the corridor could handle 150-200 million tons of cargo annually, equivalent to 4.3-5.7% of Malacca’s current capacity.

This project is particularly appealing to Vietnam, whose territorial waters are severely challenged by China’s “nine-dash line” claims in the South China Sea.

Thailand can thus assume part of Singapore's "soft power". Conversely, Thailand risks setting off a secessionary attempt in the southern part of the country.

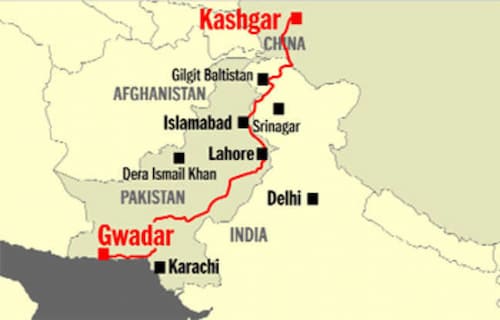

China’s Investments in Pakistan’s North-South Corridor

The China-Pakistan Economic Corridor (CPEC) is the largest and most complex BRI project to date. It centers on a railway connecting China to a new deep-water port in Gwadar, Pakistan, providing an alternative supply route bypassing Malacca.

However, the project has faced delays and significant cost overruns. Servicing BRI-related debt is a primary reason Pakistan now spends more on foreign debt repayment than on education and healthcare. Additionally, CPEC faces frequent attacks from separatist groups in northern Pakistan (e.g., Khalistan) and Gwadar (e.g., Baluchistan), requiring increasing military protection.

CPEC is partially operational and expected to be fully operational by 2030, with a projected capacity of 50-100 million tons of cargo annually, equivalent to 1.5-3.0% of Malacca’s current traffic.

Myanmar’s Bid to Become a Transit Hub

Through BRI, China is financing the China-Myanmar Economic Corridor (CMEC), which aims to establish an alternative waterway via Myanmar’s rivers to the Indian Ocean. However, this USD 10-15 billion project is significantly delayed and threatened by Myanmar’s ongoing civil war. Once completed, CMEC is expected to handle 40-50 million tons of cargo annually, about 1.3-1.5% of Malacca’s current volume.

Limited Relief, Yet Strategic Investments

In total, these alternatives to the Strait of Malacca offer only limited relief. If all projects are completed, they could handle at most 9% of Malacca’s current traffic, covering about 25% of China’s shipments through the strait.

Notably, transit through the Strait of Malacca is currently free. By investing massive sums in CPEC, CMEC, and potentially Thailand’s Landbridge project, China is prioritizing strategic returns in the form of supply chain security over economic profitability. These investments represent significant costs for limited freight savings but have immense potential for enhancing long-term supply resilience.

See also the previous and the three subsequent blog posts in this sequel on Maritime Bottlenecks.