Central banks seek greater autonomy and a more limited use of liquidity stimuli. This is the first of three monetary policy themes that could influence 2025. All three may have significant short- and long-term implications for the financial system.

The Fed Wants to Safeguard Its Independence …

Central banks operate through three main tools: liquidity (money supply), interest rates, and currency. In 2025, all three could face challenges in the United States if we project the statements made by economists and politicians in 2024:

- Central banks seek greater autonomy and less use of liquidity stimuli.

- Trump seeks influence over the Federal Open Market Committee (FOMC) decisions; see the next blog post.

- Trump wants the USD exchange rate to decline; see the last post in this trilogy.

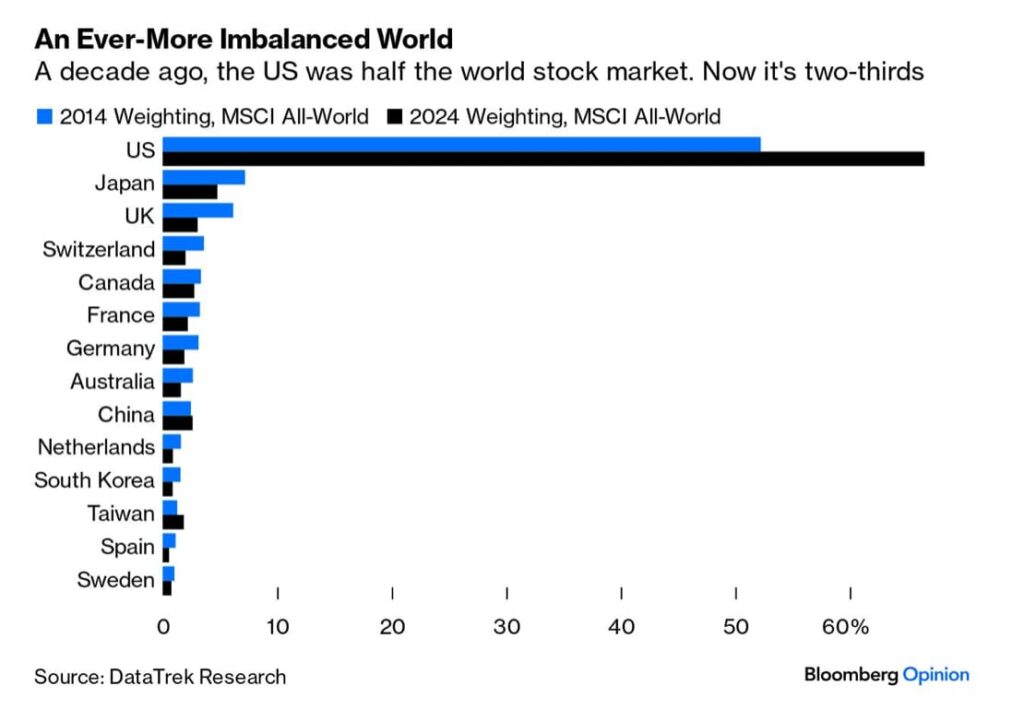

“What happens at the Fed affects the world.” The Fed’s monetary policy paradigm influences all other central banks because USD is the leading global reserve currency, the United States is the world’s largest economy, and U.S. stock markets account for nearly two-thirds of global market capitalization, see below.

… Learning From the Losses After the Inflation Spikes of 2020 and ’21 …

When inflation surged in 2020 and ’21, driven by supply-side events such as production and shipping constraints, the Fed had to raise interest rates to “get ahead of the curve” and restore market confidence. This led to significant losses on most central banks’ balance sheets, including the Fed’s.In practice, this meant that while the Fed had sent profits to the U.S. government for years through gains on its QE programs (from falling yields on the Fed’s bond holdings), a sharp reversal occurred, resulting in major losses.

These losses rendered the Fed technically insolvent and required a guarantee from the U.S. government. While this issue is theoretical in nature when issuing the world’s leading reserve currency, it dented market confidence in the Fed’s ability to foresee and manage market conditions. This loss of confidence also triggered uncomfortable dialogues with Congress and criticism from several politicians.

… Resulting in a Loss of Control and a Threat to the Fed’s Credibility

The inflation spikes of 2020 and ’21 had relatively simple causes: they were outcomes of COVID restrictions. However, no one had predicted their likelihood or the scale of their impact. This has led economists and the Fed itself to conclude that such risks must not recur. A similar supply shock could emerge from the trade war Trump has announced. For instance, China remains the primary supplier of critical minerals and metals to the U.S..

A Central Focus is Reducing Balance Sheet Risk

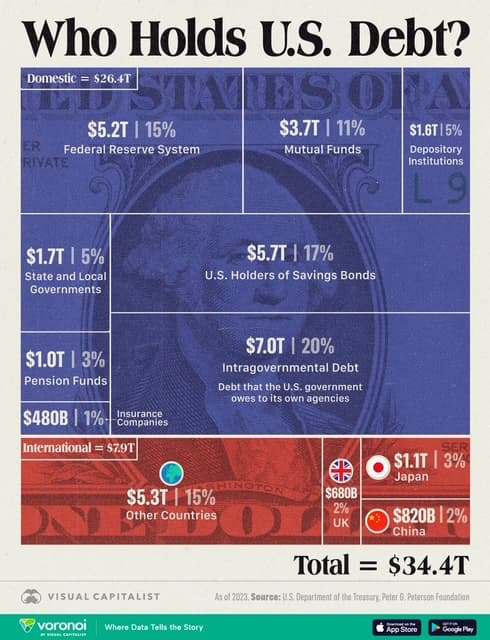

Currently, the Fed owns 15% of the government’s debt, with an additional 20% held by other government agencies, as shown below.

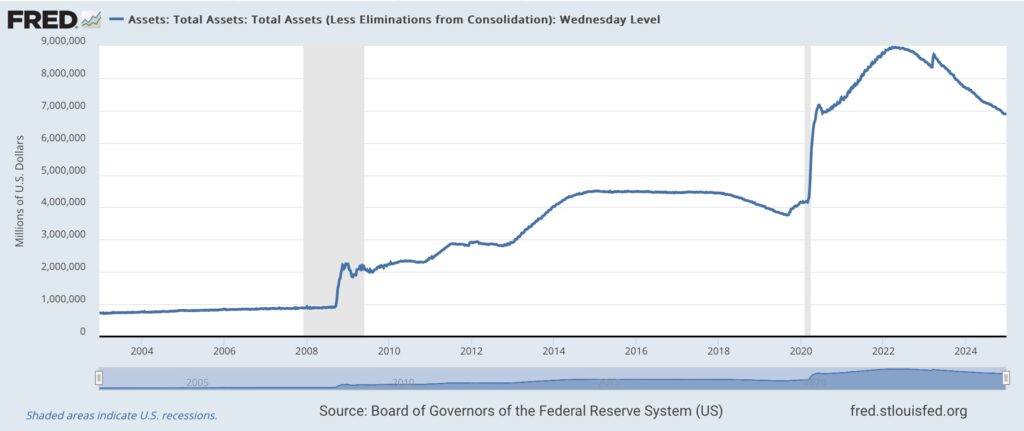

This high percentage persists despite the Fed’s quantitative tightening (QT) efforts since 2022 to reduce its balance sheet, as illustrated below.

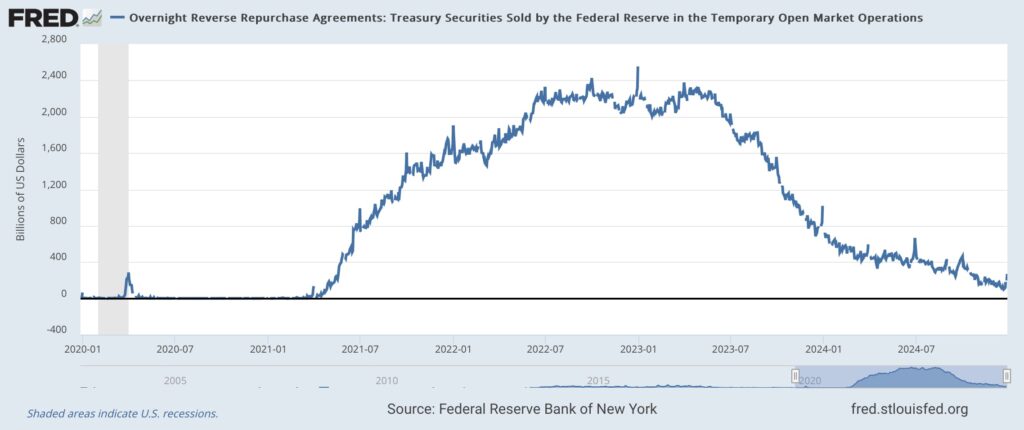

At the same time, overall market liquidity is tightening, as evidenced by the Reverse REPO mechanism described below. This is also reflected in declining bid-to-cover ratios.

… Which Will Require a Shift in the Governance Paradigm

In May, the Hoover Institute held a small monetary policy forum attended by leading economists.Former Treasury Secretary Larry Summers summarized the consensus from the meeting as follows:

- “Return to humility”: Every decade brings economic shocks. One cannot write rules to predict these but should instead view them as vents that need to be released periodically.

- “Avoid forward guidance”: Markets don’t believe it anyway, and it restricts the Fed’s future actions.

- “Use QE only to ensure financial stability, not as a tool for economic growth”: QE shortened durations and cost the U.S. half a trillion USD.

- “Avoid rigid targets wherever possible”: Credibility stems from a social consensus that low inflation is good, not whether it is 1.8% or 2.1%. Targets should be long-term and softly defined, such as an interval.

- “Avoid ambiguity”: Stop publishing summaries of FOMC deliberations and avoid speeches where FOMC members express personal opinions.

… A View Also Supported by the BIS

The consensus from the Hoover Institute meeting does not bind the independent FOMC in any way. However, it appears that the Fed and other central banks may be considering similar ideas. Since the Hoover meeting, the BIS (Bank for International Settlements) has also proposed new “guiding principles” for central banks..

These principles emphasize that central banks’ balance sheets should be as small and risk-free as possible. However, they must remain flexible.

- In practical terms, this means that liquidity operations should be highly targeted and based on much shorter durations than currently practiced.

- This approach would represent a significant departure from how central banks’ roles have evolved since the financial crisis. For example, the Fed’s near-unlimited balance sheet expansion from 2008 to 2014 was aimed at stimulating economic growth. Similarly, the ECB pursued a similar path, though Draghi’s official justification was financial stability.

Trump’s Economic Policy Depends on the Fed’s Willingness to Finance

Trump’s second presidential term will involve an economic policy based on tax cuts, financed through experimental tariffs. There is significant uncertainty about how much revenue the U.S. will actually be able to generate. This uncertainty arises partly because the last major experience with tariffs dates back to William McKinley’s presidency in the 1890s (Dingley Act). At that time, the effect on the U.S. economy was modest, and the world has changed dramatically since then. Today, U.S. trade partners know where and how the U.S. depends on their supplies, giving them considerable bargaining power.

For the Fed, this means that the uncertainty surrounding the U.S. budget deficit will become a significant issue. If financial stability is to be maintained, there must be enough buyers for U.S. Treasury bonds. This could prove difficult if the U.S. simultaneously engages in a trade war, seeks to weaken the USD exchange rate, and introduces political control over FOMC decisions. See the next blog post.